For the last two years, many potential American homebuyers have found themselves priced out of the market. Soaring interest rates and prices for construction materials, along with a sharp decline in supply from a decade-long building slowdown, have inflated the cost of buying housing far more than family incomes have gone up. One recent study found that median housing prices in hundreds of U.S. counties were now so high that an average buyer would need to spend more than 38 percent of his earnings on monthly housing payments—a greater proportion than at any time since the early 1980s. Renters haven’t escaped the pain: more than half of Americans now surrender over 30 percent of their income on rent. The crisis has led to calls for more government-led, taxpayer-paid building projects, via “affordable-housing” programs. In last November’s elections, several communities approved new taxes to finance such subsidized home building. More local proposals are in the works, too, and an already-bloated federal government is intensifying its own commitment to Washington-directed affordable housing.

The one thing that these efforts are unlikely to accomplish, though, is easing housing woes. Government-led affordable housing tends to be pricey and cumbersome to construct, and it ignores a main source of our housing difficulties: local government rules that make it increasingly unprofitable for the private sector to construct homes efficiently and quickly. That supply-side failure, reinforced by misguided federal fiscal and monetary policy that drove interest rates up in early 2022, has produced the current predicament. Reforms that let builders build more—especially as interest rates fall—should be a far greater priority than unwieldly government housing projects that burn tax dollars, tie up construction jobs, and have logged a long history of grand promises, underperformance, and fraud.

Finally, a reason to check your email.

Sign up for our free newsletter today.

Seattle voters jumped into the fray in November 2023, passing a supplemental real-estate tax to raise up to $930 million to expand the city’s affordable-housing supply. Santa Fe residents approved a 3 percent “mansion tax” for affordable housing that applies to houses sold for more than $1 million, while Boulder County voters in Colorado renewed a sales tax, created specifically to fund affordable housing, to the tune of $15 million to $20 million annually. Los Angeles passed a mansion tax in 2022, with some of the funds allocated to new housing for the homeless. While voters recently rejected Chicago mayor Brandon Johnson’s proposed mansion tax, which would have tripled the levy on sales of residential properties valued above $1 million, Boston’s mayor is pushing the Massachusetts state legislature to impose a similar tax on sales of properties valued over $2 million.

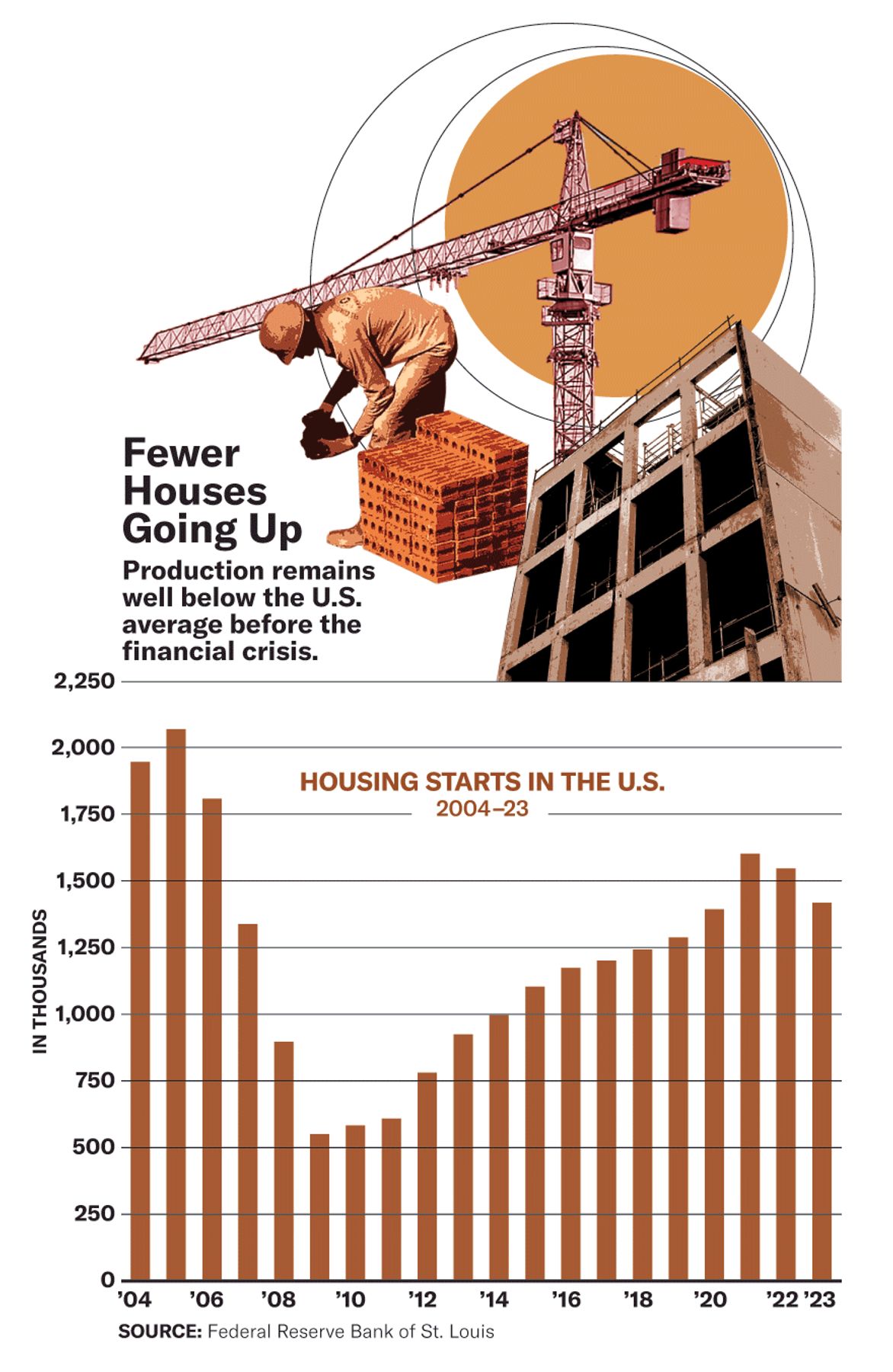

Advocates for the taxes argue that private developers focus too much on luxury homes. But the real culprit for the high prices is that housing production in many communities cratered. The collapse started more than a decade ago and has hit prices up and down the scale. The immediate cause was the 2008 meltdown in America’s mortgage industry. Government pressure on lenders to weaken underwriting standards, and thereby expand homeownership, helped trigger the disaster, as many people took on mortgages that they couldn’t repay. But thickening local building barriers—especially zoning that limits many forms of residential construction—made matters far worse. One recent study found that big cities that restricted denser housing imposed a steep “zoning tax” that constrains the supply, and inflates the overall price, of new housing. That tax climbs as high as $500,000 per acre in New York City, $400,000 in San Francisco and Chicago, and $200,000–$300,000 in Seattle and Philadelphia. Yet, even as housing construction has plummeted, some local governments have come up with even more ways to block it, such as the creation of dubious “preservation” districts, which freeze neighborhoods against most change.

The housing implosion is truly eye-opening. For ten years, starting in 2009, U.S. builders erected only about 860,000 new units annually, compared with 1.7 million yearly in the decade precrisis. That left the country with 5 million–8 million fewer units than it might otherwise have had available. Even after the recovery began, housing production stayed well below what the nation averaged in the 30 years pre-2009.

The breakdown is especially notable in markets enacting new levies to build taxpayer-subsidized housing. Boulder County officials had urged citizens to reapprove its affordable-housing tax to meet the needs of lower- and middle-income residents. But the area’s real problem is a major home-building contraction. Since the housing bust, the county has averaged only about 1,300 new units a year, compared with more than 3,000 annually in the 1990s. Santa Fe has suffered an even more striking decline. In the decade before the mortgage-market crisis, the county issued more than 6,100 permits for new housing. In the decade following, that number slumped to just 1,283. That translates into a massive reduction of new units built.

Builders finally began to rebound from the mortgage crash in the late 2010s, but then Covid-19 struck. Pandemic shutdowns disrupted things again, re-intensifying the supply crunch. When interest rates spiked in early 2022, sending the rate on a 30-year fixed mortgage from under 3 percent in 2021 to 6.8 percent last year, the percentage of U.S. households that could afford to buy a home fell to a record low—leading to more pleas for subsidized government housing programs.

Appeals for government intervention ignore the manifold problems with taxpayer-funded affordable-housing initiatives. A recent Government Accountability Office report examined the performance of the federal housing trust fund, which subsidizes affordable-housing plans. Since 2015, the fund has received some $3 billion for housing projects; as of March 2022, developers had finished just 2,186 units nationwide. The program churns out only 400 or so units quarterly, a vanishingly small number, given the national need. Construction costs are outrageously high, too, averaging as much as $360,000 per unit in California, $339,000 in New York, and $314,000 in Massachusetts.

And the GAO report understates the problem where it is most acute. Affordable-housing projects in California, where many metros face a desperate housing shortage and government is pouring hundreds of millions of dollars into subsidized building, have scaled as high as $1 million per unit, a Los Angeles Times investigation found. Though supply problems and labor costs have gone up, the Times found that government rules and regulations were major factors in construction projects that made a mockery of the term “affordable housing.” “In comparison with private sector development, low-income housing is often saddled with more stringent environmental and labor standards,” the newspaper noted. “Affordable housing projects also frequently face high parking requirements, lengthy local approval processes, and a byzantine bureaucracy to secure financing.”

Among the costs were requirements that builders pay workers union-level wages—a mandate that increased prices by up to $50,000 per unit, one study found. Stricter environmental rules added up to $17,000 per unit. As much as 14 percent of the cost of the affordable-housing projects goes to consultant fees, including for attorneys and other experts necessary to navigate convoluted government regulations. Some California projects require developers to include “public art.” By contrast, a private developer who rejected government funding for a South Los Angeles project was able to build low-income housing for $291,000 per unit because the project didn’t have to adhere to regulations that govern public subsidized construction.

Fiscal mismanagement has plagued such initiatives. A federal affordable-housing program on Indian reservations, for instance, spent $800 million in taxpayer money to construct 1,110 units, a cost of about $720,000 per unit—more than double the median sale price of houses in the Arizona districts where the building took place.

Developers on these projects too often abuse public trust because they aren’t spending their own money. In one egregious Miami case, four developers specializing in affordable housing pled guilty to overcharging the government by some $34 million on 14 projects. More than half of all projects that the GAO examined in one report had never undertaken a required audit. The government plans, the report said, were susceptible to overcharges for work, or charges for work that never happened, and landlords sometimes slapped tenants with rents above what the programs officially allowed.

Government-subsidized housing also demands that agencies and developers stick to strict standards when renting or selling these units, once built. But the oversight is also often lacking. New York officials recently indicted several developers for collecting $1.6 million in tax credits for affordable-housing projects that they had never bothered renting to qualified applicants. Some tenants can get wealthy from the lack of scrutiny. A New York State comptroller study found 230 subsidized-housing units occupied by tenants earning hundreds of thousands of dollars annually in income—including one earning over $1 million. Project administrators, the report observed, hadn’t bothered checking on these tenants’ eligibility in years.

These abuses underscore how government-backed affordable housing distorts the marketplace, especially in heavily regulated cities like New York or Los Angeles, where it’s otherwise tough to build anything. In a free market, renters with growing incomes would normally move out of their subsidized places and into bigger and better housing, clearing the way for new tenants. But in a constrained market, the cost of an unsubsidized house or apartment can be so great that even well-off renters often stick it out in government-bankrolled leases, preventing the turnover typical of a vibrant housing sector.

Even absent fraud, government housing programs build inefficiently. In Seattle, a 2016 property-tax hike to fund affordable housing, worth $290 million over seven years, has produced just 2,741 units—in a metro area that needs roughly 17,000 new housing units annually to make up for its housing shortfall.

Meantime, tax hikes to fund cheaper housing may depress sales, again suppressing the turnover that frees units for others. That’s particularly true of mansion taxes. One study on capital-gains taxes, which apply to houses sold for more than $500,000, found that every $10,000 increase in taxes on these sales reduced annual real-estate transactions by 6 percent to 13 percent. Los Angeles’s mansion tax, projected to raise $900 million annually, has brought in less than $200 million in its first year, as sales have struggled. “You don’t have as many buyers out there trying to buy; we don’t have as many sellers willing to sell,” an agent told viewers of the Netflix reality series Selling Sunset, which chronicles the go-go world of luxury real estate in Los Angeles. Further, broad-based mansion taxes like L.A.’s also hit multiunit apartment buildings, potentially adding tens of thousands of dollars to their purchase price—hurting their value, diminishing owners’ ability to maintain them, and adding pressure to raise rents.

Recent research by Evan Mast, published in the Journal of Urban Economics, has shown that adding new housing supply, even at the high end, unleashes a ripple effect that opens more housing across the income spectrum. For every 100 renters moving into new, market-rate housing in an area, Mast found, 45–70 other renters move up into the units they vacated, in turn freeing up their own, less expensive, units. As a study from New York University’s Furman Center put it: “[A]dding new homes moderates price increases and therefore makes housing more affordable to low- and moderate-income families.”

Places where construction has ramped up, moreover, are seeing prices fall—a reminder of how supply and demand works. Cities like Phoenix and Atlanta have added more than 16,000 housing units over the last year, and seen rents drop 4.5 percent and 4.1 percent, respectively, even with inflation still elevated. Why are developers building in these places? One reason is certainly that, as research shows, these markets have virtually no government-imposed zoning tax. By contrast, according to a Bloomberg analysis, rents continue to rise in places with constrained supply. Rochester, New York, has expanded its number of housing units by just 0.3 percent; prices are up 5.5 percent. And rents have jumped 8.7 percent in Springfield, Massachusetts, where no significant overall addition to the area’s housing stock has occurred, Bloomberg found.

City officials in some places have started to revise their zoning and permitting process to fast-track projects and allow bigger, denser building. Minneapolis, an early reformer, allowed builders to construct more multifamily dwellings in areas that previously banned them. The efforts were controversial, with many homeowners fearing that ambitious builders would rip down single-family houses in favor of bigger multifamily structures that would transform their communities. That hasn’t happened, which isn’t surprising, as such teardowns and rebuilds aren’t economical. Instead, planning changes that encouraged builders to add more housing in corridors with available public transit have set off a housing boom. Over the past five years, the city has permitted even more new units annually than during the roaring years before the 2008 financial crash. Rents relative to average incomes in the area have dipped 20 percent.

The Minneapolis story offers a lesson in how to navigate housing reforms. In many places, officials have focused largely on rewriting zoning laws in ways that seem targeted at eliminating or remaking communities of single-family houses—exactly why they have faced heated opposition. But such reforms aren’t doing much to ease the housing crisis, anyway, as merely taking small, single-family plots and creating three- or four-unit new housing on them doesn’t add much to supply. A survey in California a year after the passage of SB 9, a law that lets homeowners create up to four units on a single-family plot, found that only 53 new units had been approved in 13 cities under its provisions.

By contrast, updating codes to give builders greater freedom to erect residential projects is what has worked best to stimulate new housing. Such a change might also give a boost to the construction industry. Building restrictions enacted in many cities over recent decades have turned construction into a small-time endeavor, dominated by tiny local firms—contributing to a slowdown in the industry’s productivity. According to research by economists Austan Goolsbee and Chad Syverson, builders have taken a “strange and awful path of productivity” for the last half-century. Before 1970, the industry produced at a greater rate than the overall U.S. economy. Since then, its productivity has declined by an average of 1 percent per year, a “stunningly bad” performance for a major sector, and one that has had a negative impact on housing affordability, the authors write.

One offender in this decline, according to Harvard economist Edward L. Glaeser and business executive Atta Tarki: zoning limits that restrict larger building projects. Much of affordable housing fits into that category. “The timing of the drop in [construction industry] productivity reflects zoning changes that shut out large companies,” Glaeser and Tarki observe. “Land-use regulations really began to limit large-scale housing production in the 1960s, making the sector less conducive to bigger companies. Small-scale housing projects don’t enjoy scale economies, and small housing producers don’t have the resources to invest in the research and development that can lower costs.” Reversing this process and enabling big projects of the type typical during the post–World War II building surge—exemplified by developments like Levittown, on Long Island—require a comprehensive metro plan, one that looks to make such large-scale projects easier in places where they’re desirable.

Still, the growing enthusiasm for government-subsidized housing won’t make it easy to unleash the private sector. Part of that momentum now comes from a powerful coalition of homeless advocacy groups, allied with progressive politicians, who link homelessness to steepening housing prices, which, they contend, force people to live on the streets. That premise lies behind plans for ambitious building programs aimed at providing government-subsidized housing for the homeless in places like California—a state that now has some 181,000 homeless.

Such plans misdiagnose the problem. According to federal data, the number of homeless in America is no greater today than in 2007, the year before the crash that stifled housing production. In much of America, homelessness has fallen since then. Only a handful of states—notably, California, New York, Oregon, and Washington—have seen substantial increases in their homeless population. Much of that is a function not of high housing costs but of rising social disorder, fueled by bad government policy—the decriminalization of drug use, federal court rulings and local laws that make it hard to dismantle outdoor encampments, and “harm reduction” strategies that allow drug users to maintain their habits under government supervision in “safe injection sites.” Coexistent with this has been the rise of “housing first” policies, which advocate for curing homelessness by getting people into government-subsidized housing, without addressing the mental-health and addiction problems that typically made them homeless in the first place. The result of these misguided measures has been an increase of nearly 43,000 homeless in California and almost 41,000 in New York since 2007, even as the number of people without housing in places like Florida, Texas, and Georgia has shrunk over that period.

Los Angeles mayor Karen Bass recently lamented the slow pace of government-backed affordable-housing construction in her city. “How on earth could we expect to house 40,000 [homeless] people if we continue to do business as usual?” she asked. That Bass ever supposed government could create 40,000 units of housing for the homeless, or that she thinks housing so many troubled people in massive government projects would be a good idea, shows how out of touch some officials can be in housing policy. Without a major shift in thinking, the result will be billions more dollars squandered—and a housing crisis still unsolved.

Top Photo: A YMCA in Chicago being converted to affordable housing. The city’s mayor has proposed a tax on high-end residential real-estate sales to fund a subsidized-housing program—though voters have balked at his plans. (Kamil Krzaczynski/ Walker & Dunlop/AP Images)