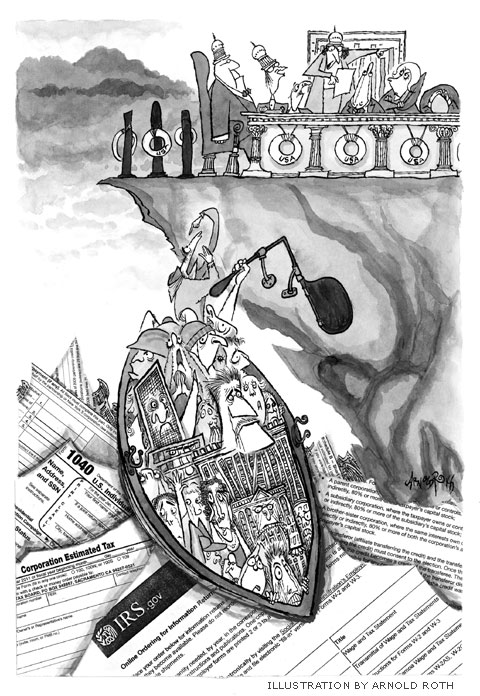

Warren Buffett is worried that he doesn’t pay enough in taxes. In an August op-ed in the New York Times, the billionaire pointed out that his effective federal tax rate—the percentage of all his income that he paid in federal tax—was just 17.4 percent. The reason for Buffett’s light burden is that he gets so much of his income from investments in company stocks, which are taxed comparatively lightly: while the federal tax rate for wage income can rise as high as 35 percent, most income from stocks is taxed at a flat 15 percent.

Seizing on Buffett’s complaint, President Barack Obama has proposed the “Buffett Rule,” which would compel millionaires to pay as great a share of their incomes as lower earners do, effectively taxing their capital gains and dividends more. It’s easy to see the intuitive appeal of raising taxes on capital income. Also in August, business columnist James Stewart wrote in the Times that “simple fairness” was the best argument for taxing capital gains at ordinary income rates. He quoted economist Leonard Burman: “In my experience earning income from capital gains is a lot easier than earning ordinary income. Why not tax both at the same rate? It only seems fair.” Most tax-reform proposals today likewise seek to raise taxes on capital.

Finally, a reason to check your email.

Sign up for our free newsletter today.

What they seem not to understand, though, is that the current tax code doesn’t reward investing in capital; it punishes it. By further discouraging the investment that the recession-damaged economy needs to innovate and grow, the Buffett Rule would take the tax code in exactly the wrong direction. For the good of the country, as surprising as it may sound, Warren Buffett ought to get a tax cut.

Buffett’s 17.4 percent claim is deceptive. While the figure includes his personal income tax, as well as payroll taxes for Medicare and Social Security, it doesn’t include another levy that he pays, albeit indirectly: the corporate income tax. The money that Buffett makes as an investor is simply a share of the profits of the companies whose stock he owns. Those companies have already paid the corporate income tax—as much as 35 percent of their incomes—which dramatically reduces their profits, and thus Buffett’s take.

Another way of looking at this is to remember that a shareholder is a part owner of a company. In the current tax system, he’s essentially paying taxes twice: first as corporate income tax, and second as personal capital-gains or dividend tax. Because of this double taxation, the tax code winds up treating investing less favorably than labor. In 2005, the Congressional Budget Office, adding together the corporate- and personal-level taxes, estimated that the total federal tax burden on capital investments in corporations was 26.3 percent. Personal income and payroll taxes, by contrast, accounted for just 17 percent of personal income that year.

That Buffett pays way more than 17.4 percent in federal levies, once you include the corporate income tax, is less important than what the double-taxing of capital does to the economy: it gives people an incentive to shift their money from investing to consumption. One of the biggest problems that the U.S. economy struggles with is too much spending and too little saving and investing; the tax code should work against this trend, not exacerbate it.

Our current tax system introduces a further distortion by allowing corporations, when they issue debt, to deduct the interest payments from their taxable income. These deductions are so valuable that the total federal tax burden on corporate debt is negative 6.3 percent, according to the CBO—meaning that corporations receive a subsidy for their debt-financed activities. This subsidy spurs them to finance themselves more with debt and less with equity, increasing the risk of corporate bankruptcy.

Obama’s Buffett Rule would worsen both the double-taxing problem and the debt-subsidy problem. Hiking personal income-tax rates on capital-gains and dividend income, as the rule would require, would give potential investors even more reason not to invest. And because it would mainly affect taxation of stocks, not bonds, it would increase the disparity between the two, further encouraging companies to issue debt. Nor is Obama alone. Many recent bipartisan tax plans, including the generally sensible one developed by the White House’s fiscal commission, headed by Erskine Bowles and Alan Simpson, have called for taxing dividend and capital-gains income at the same rates as wage income.

Why are today’s tax reformers pushing in the wrong direction on capital taxation? There’s the fairness argument, of course, and also its cousin, the progressive argument: because people with high incomes disproportionately receive capital income, less favorable treatment of capital tends to make the tax code more progressive (at least if you assume that the tax burden on capital is borne solely by investors and not by companies’ employees and consumers, who will have to shoulder lower salaries and higher costs).

Some reformers, too, want to tax investments at higher rates so that they can lower the top individual tax rate on wage income. One option that the Bowles-Simpson plan proposes, for example, reduces the top rate on all income to 23 percent and still raises more revenue than today’s tax code does. But it can only accomplish that feat because it hikes capital-gains and dividend taxes while leaving corporate income taxes in place, though at a somewhat reduced rate. The Bowles-Simpson plan’s true effective tax rate on investment would be higher than today’s—well over 30 percent.

Race to the Financial Bottom

In late September, European Commission president José Barroso unveiled a new idea: a tax on financial transactions throughout the Continent and Britain. The goal is to raise $77 billion annually, starting in 2014. But the tax would also, warned Michael Spencer, chief of the derivatives giant ICAP, “destroy the City”—the City of London, that is, Britain’s equivalent of Wall Street.

Ordinarily, such a tax would be a gift to New York City, which would welcome derivatives traders and asset-management firms fleeing a suddenly hostile Europe. New York learned its lesson about these taxes 30 years ago, when it killed a tax on stock transactions because it was driving business from Manhattan. No New York politician has gotten far by proposing that it be reinstated. The last mayoral candidate who tried, former Bronx borough president Fernando Ferrer, lost badly to Michael Bloomberg in the 2005 mayoral election.

But America’s confused attitude toward finance weakens the incentive for overseas financiers to move west. President Obama’s Buffett Rule would hike tax rates on capital gains and dividends for wealthier Americans. Obama hasn’t said how high he’d like to raise the rate from today’s 15 percent, so derivatives market makers and asset managers, who don’t like uncertainty, won’t find a more predictable investment climate in New York.

Another, bigger problem is that America has failed to take the lead in choosing sober regulation of the financial industry over punitive taxation. Obama has fallen into the same trap that snared Barroso, who justified the proposed tax by saying, “It’s a question of fairness. It is time for the financial sector to make a contribution back to society.” But banks can’t pay a tax to correct the real unfairness infecting capital markets: the fact that banks are unable to take big losses on their bad investments without dragging everyone else down with them. It is government’s job to limit borrowing and interconnectedness within the financial sector, so that firms can go under without risking a depression.

Western dithering on this front stalks the recovery. It drives everything from the European sovereign-debt debacle to the Occupy Wall Street protest in downtown Manhattan. By concentrating his rhetoric on superrich investors who should pay their fair share, Obama confuses two separate issues—financial regulation and tax reform—without adequately addressing either. Republicans are just as bad, with congressional members criticizing derivatives regulations that would make the system safer but that might drive up costs for big businesses. The GOP should realize that low taxes don’t help the economy when one badly regulated industry, thanks to its ability to take the economy hostage, dominates others.

American and European leaders still have time to choose strong rules to govern finance and to couple them with predictable tax rates. By choosing correctly, either Europe or America can become a haven for financial firms unafraid of free-market capitalism.

—Nicole Gelinas

A better tax-reform plan would cut tax rates on capital, rather than simply cutting tax rates broadly. A key principle of this approach: all income would be taxed only once, so that people’s and businesses’ decisions would be distorted as little as possible.

There are a few ways of achieving such neutrality. One, recommended by staff at the Treasury Department in the 1990s, is the adoption of a comprehensive business income tax (CBIT). Under this system, businesses would no longer be allowed to deduct their interest expenses from their taxable income, but individual investors and bondholders—the people ultimately receiving that business income, whether from stocks or from bonds—wouldn’t have to pay taxes on it. So the money would be taxed just once. Further, because the CBIT would apply equally to corporate debt and corporate equity, it would remove companies’ incentive to borrow too much. However, a CBIT would make it impossible to tax capital income progressively: since the single tax would be paid at the corporate level, wealthier shareholders and bondholders couldn’t be made to pay more.

Another option, widely used in other Western countries, is an “imputation-credit” system. Corporations would still pay income taxes, but those who received dividends from those corporations would then deduct the corporate taxes from their taxable income. In many cases, such a rule is the equivalent of eliminating taxes on dividends.

A third option would be to stop taxing income entirely and to tax consumption instead. New York University professor David Bradford suggested a system called the “X tax,” in which both businesses and individuals would pay an income tax—but individuals, crucially, would pay no tax on interest, dividends, or capital gains. Since people can do only two things with their income—invest it or spend it—a government that taxes income without taxing capital is imposing the equivalent of a consumption tax. The businesses, meanwhile, would pay taxes on the revenue that they took in from customers—again, this would be a consumption tax—but subtract from their taxable income whatever they bought from other businesses, as well as what they paid their employees. Though its operation is significantly different, the base of the X tax is the same as that of a value-added tax (VAT). But unlike with a VAT, the government could levy tax at lower rates for lower-wage individual earners, introducing progressivity and potentially drawing some Democratic support to the plan.

Any of these reforms, of course, would bear a price, since the government would lose revenue by no longer double-taxing capital. To help make up for the gap, the top tax rate on individual wage income, for starters, would need to remain in the neighborhood of today’s 35 percent rate, instead of the much lower rates envisioned in the Bowles-Simpson plan. But by eliminating various tax credits and deductions, such as the deductions for state and local taxes paid and for mortgage interest, the government could pay for reform and even afford to set lower rates for lower- and middle-income earners. Better still, it could increase the earned income tax credit, a benefit that the very lowest wage earners receive.

Because these reforms would reduce or even eliminate the taxes that investors pay on capital income, Warren Buffett’s tax bill would be smaller than it is today. Some other investors with extremely high incomes would likewise be better off. But the tax burden wouldn’t be shifted to the middle class and the poor. Rather, the brunt would be borne by wage earners in the top quintile—partners in law firms and corporate executives, for instance—who have labor income taxed in the top bracket and who tend to benefit heavily from tax deductions.

If you think that tax reform should be solely about lower marginal rates, none of these proposals will be music to your ears. It’s important to remember, though, that one reason that we care about lowering marginal tax rates is that higher rates squelch economic activity—and capital is more sensitive to that effect than labor is, in part because capital can so easily flee to lower-tax jurisdictions. Tax the income of a corporate lawyer, and he’ll probably keep working, at least up to a certain point. Tax the stocks of an investor, and he may consider investing in firms located abroad, thus avoiding the corporate tax altogether and depriving the U.S. of investment capital.

This broad principle of reform—lower taxes on investment income, financed with taxes on labor income earned by the affluent—could appeal to both sides of the aisle. Such a big change may look like a heavy lift. But it’s worth remembering that the Tax Reform Act of 1986, which made many useful changes to the tax system, looked impossible until it became law. Better policy may be more feasible than it appears. And the long-term economic effects of reform along these lines would be profound: better incentives for business investment and job creation, fewer incentives for businesses and individuals to pile up debt—and faster long-run economic growth.