As the highly inflationary Inflation Reduction Act passes its first birthday, it’s worth taking stock of its track record over the last 12 months.

First, in contrast with its name, the IRA hasn’t done much to reduce inflation. Even President Biden agrees, now that political attention is focused elsewhere. “It has nothing to do with inflation,” Biden told donors recently, conceding what critics said all along. “It has to do with the $368 billion, the single-largest investment in climate change anywhere in the world.”

Finally, a reason to check your email.

Sign up for our free newsletter today.

Economists know that policy should “lean against the wind” of the economic cycle, adding fiscal and monetary support when the economy is weak and has too little inflation, and removing that support when the economy is strong and experiencing high inflation. In that sense, with inflation recently running as hot as 9 percent, this was the worst possible timing over the last four decades for new fiscal money; if the IRA really aimed to reduce inflation, it would have removed fiscal money from the economy, not injected more.

True, the IRA has promised some reductions in deficits, but they’re either backloaded into the second half of the five-year window (by which time, presumably, inflation will no longer be a significant concern), or they’re hypothetical, as with the expectation that an increased IRS budget will bring in more revenues. Taxpayers have been disappointed in the past, receiving no better government performance in exchange for fatter budgets.

Second, not only did the IRA boost demand in an already-overheated economy; it also further distorted the supply side, worsening inflationary pressures. The original Congressional Budget Office estimate for the size of the IRA’s environmental tax credits came in at just under $300 billion, but recently revised estimates from the Joint Committee on Taxation put that number over twice the original score. This newer estimate would wipe out all the net expected deficit reduction over the entire budget window.

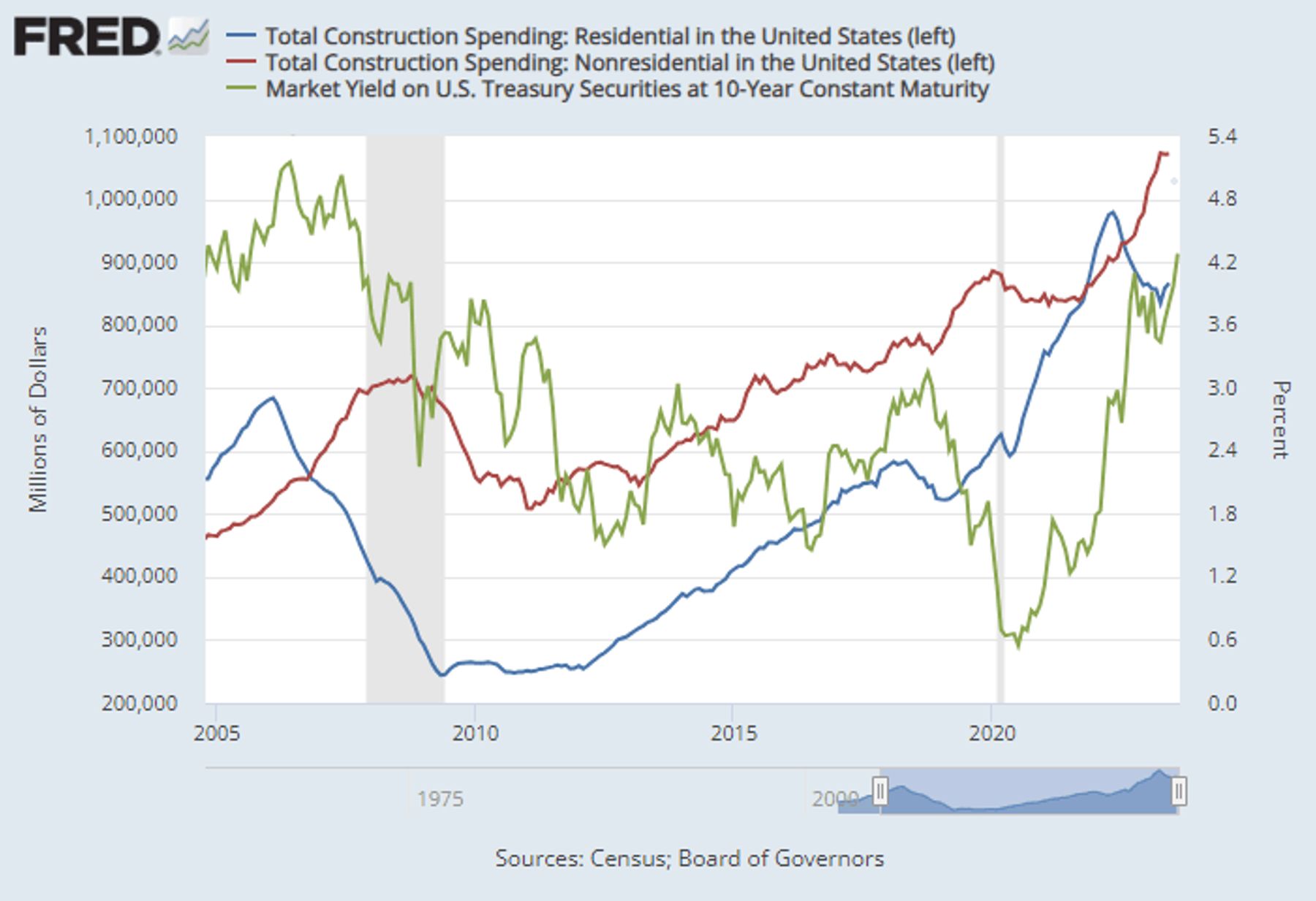

These subsidies have led to a boom in nonresidential construction activity as companies rush to take advantage of the tax benefits, building factories for everything from electric vehicle batteries to chemical refining facilities that are key inputs into the “green supply chain.” It should be no surprise that if the government funnels hundreds of billions of dollars into a sector, then economic activity in that sector would rise. Nonresidential construction has rocketed higher, and nonresidential investment contributed about 1 percent of the 2.4 percent expansion in the economy in the second quarter.

The distortion of the economy lies in the activity not being sufficiently profitable without the government subsidy; if people wanted to pay full price for electric vehicles, they wouldn’t need the $7,500 credit from the government. Instead, government is redirecting activity to the economically unprofitable sector, warping the economy into something that will deliver, in the long run, less prosperity for everyone.

Meantime, to pay for the IRA and its other excessive obligations, the Treasury has had to begin issuing shocking volumes of Treasury bonds. In the second half of this year, alone, Treasury expects to borrow almost $1.9 trillion from markets, roughly half of which represents new borrowing. These eye-popping numbers have forced interest rates up, with yields on ten-year T-notes rising above the highs from last October and clocking in at levels not seen since 2007. The increase has driven the national average mortgage rate over 7.5 percent, putting home purchases beyond the reach of many families.

Largely due to the rise in mortgage rates, real residential investment is down 16 percent over the last year. This process—things that get subsidized enjoy a bonanza, and things that don’t get subsidized become unaffordable and languish—is the classic process of fiscal policy “crowding out” organic economic activity. By directing resources toward industries that are inherently unprofitable without government subsidies—those favored by the IRA—and reducing resources for other activities, government policy ensures that the supply side of the economy is heavily distorted, aggravating inflation pressures in the short run and potentially leading to bankruptcies or creating zombie firms in the long run if government support is removed. Crowding out hampers the long-run growth potential of the economy as it enlarges the share of sectors that are viable only with government support.

Industrial policy has an important place in the toolkit of government and is responsible for many of the great technological advancements—from GPS to the Internet—that kept the United States at the forefront of economic growth and strength for decades. But industrial policy must be evaluated with respect to a national goal: in the earlier examples, that goal was superiority in defense technology, aimed at winning the geopolitical struggle with the Soviet Union, so that industrial policy was a servant of national security requirements. Industrial policy aimed at our emerging geopolitical struggle with China, particularly in the telecom and defense technology spaces, would be worthwhile, if implemented prudently.

As for the IRA: its first façade was that it aimed at inflation. Its second façade was that it aimed at climate change. But does it actually address climate change?

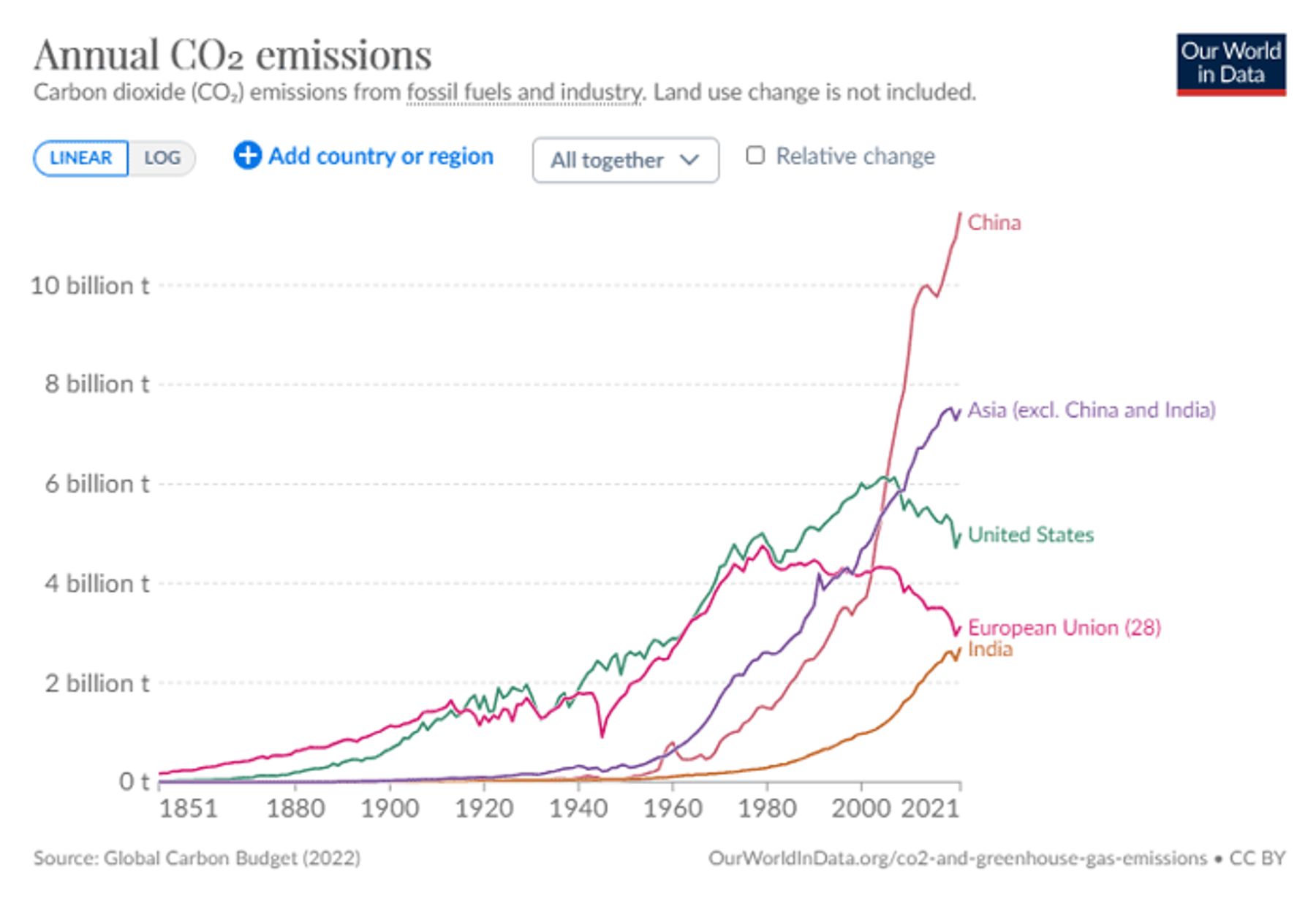

Scientists agree that climate change is affected by the global stock of greenhouse gases, not the local stock. It doesn’t matter whether carbon emissions occur in Boise or Beijing, Des Moines or Delhi; the climate effect is the same. While the investments from the IRA might reduce U.S. emissions over time, it avails nothing if those emissions are immediately replaced by emissions from other countries.

And indeed, that’s exactly what’s been happening. U.S. emissions have been in decline since the mid-2000s, in large part due to increased natural gas usage, and European emissions have been in decline since the early 1980s. Any additional climate space created by reductions in Western emissions has immediately been offset by growing emissions from the rest of the world, particularly China, whose emissions have tripled in the last two decades.

The Biden administration’s Department of Energy estimates that the IRA and the Infrastructure Investment and Jobs Act will together reduce U.S. emissions by 1 billion metric tons. But the average increase in total Asian emissions in the last two decades is 0.61 billion metric tons per year, meaning that the cumulative ten-year impact of the IRA (and the infrastructure investments) will be erased within two years. Any attempt to take emissions growth seriously must at a minimum arrest the rise in Chinese emissions, if not reverse its dramatic growth. The IRA may or may not be nobly intentioned, but it doesn’t even begin to move the needle on climate change.

What, then, can we conclude about the Inflation Reduction Act? It made substantial contributions to the biggest inflation crisis in four decades via procyclical fiscal stimulus; it directed economic activity toward unviable sectors of the economy that can’t survive without government support; it made credit for non-subsidized sectors significantly more expensive, depriving them of needed funding; and despite its intent to cut the deficit in the back half of its ten-year window, as cost estimates for the subsidies increase, it appears that it will on net add to the government debt, costing the government valuable fiscal space to deal with future crises and deepening our ruinous debt path.

And all for nothing.

Photo by Kent Nishimura / Los Angeles Times via Getty Images