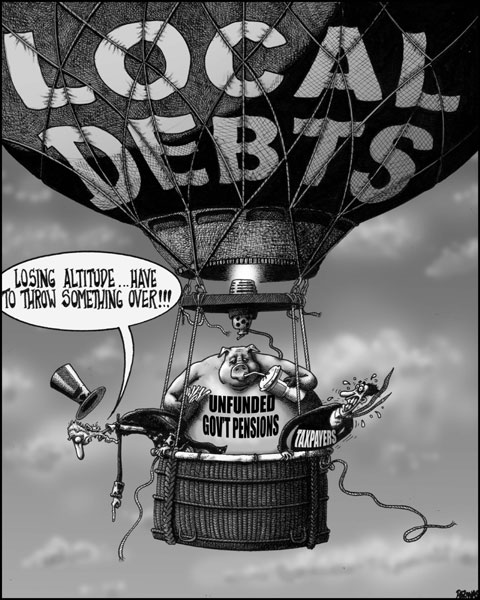

Maria Pappas, the treasurer of Cook County, Illinois, got tired of being asked why local taxes kept rising. Betting that the answer involved the debt that state and local governments were accumulating, she began a quest to figure out how much county residents owed. It wasn’t easy. In some jurisdictions, officials said that they didn’t know; in others, they stonewalled. Pappas’s first report, issued in 2010, estimated the total state and local debt at $56 billion for the county’s 5.6 million residents. Two years later, after further investigation, the figure had risen to a frightening $140 billion, shocking residents and officials alike. “Nobody knew the numbers because local governments don’t like to show how badly they are doing,” Pappas observed.

Since Pappas began her project to tally Cook County’s hidden debt, she has found lots of company. Across America, elected officials, taxpayer groups, and other researchers have launched a forensic accounting of state and municipal debt, and their fact-finding mission is rewriting the country’s balance sheet. Just a few years ago, most experts estimated that state and local governments owed about $2.5 trillion, mostly in the form of municipal bonds and other debt securities. But late last year, the States Project, a joint venture of Harvard’s Institute of Politics and the University of Pennsylvania’s Fels Institute of Government, projected that if you also count promises made to retired government workers and money borrowed without taxpayer approval, the figure might be higher than $7 trillion.

Finally, a reason to check your email.

Sign up for our free newsletter today.

Most states have restrictions on debt and prohibitions against running deficits. But these rules have been no match for state and local governments, which have exploited loopholes and employed deceptive accounting standards in order to keep running up debt. The jaw-dropping costs of these evasions have already started to weigh on budgets; as the burden grows heavier, taxpayers may decide that it’s time for a new fiscal revolt.

Most state constitutions and many local-government charters regulate public debt precisely because of past abuses. In the early nineteenth century, after New York built the Erie Canal with borrowed funds, other states rushed to make similar debt-financed investments in toll roads, bridges, and canals—projects designed to take advantage of an expanding economy. But when the nation’s economy fell into a deep recession in 1837, many of the projects failed, and tax revenues cratered as well, prompting eight states and territories to default on their debt. Stung by losses, European markets stopped lending even to solvent American states. The debacle inspired a sharp reevaluation of the role of state governments, with voters looking “more skeptically” on legislative borrowing, wrote political scientist Alasdair Roberts in 2010 in the academic journal Intereconomics. A member of New York’s 1846 constitutional convention even warned that “unless some check was placed upon this dangerous power to contract debt, representative government could not long endure.” Over a 15-year period, 19 states wrote debt limitations into their constitutions.

Since then, the history of state and local debt has been a tug-of-war between those struggling to keep governments from overextending themselves and elected officials seeking legal loopholes for further debt spending. In the second half of the nineteenth century, for instance, some states, now restricted from doing it themselves, used local governments to float debt, producing tens of millions of dollars in new obligations—and calls for limits on local borrowing. The go-go 1920s, a period of unprecedented construction and transformation throughout America, saw states and localities once again borrowing massively, this time to build roads and electrical infrastructure. State and local debt had hit $15 billion ($260 billion in today’s dollars) by the Great Depression’s onset. Arkansas was one of the heaviest borrowers, with obligations reaching $160 million ($2.8 billion today). It defaulted in 1933—one of more than 4,700 Depression-era defaults by state and local government entities, including nearly 900 by school districts.

The wave of bad borrowing led some states to tighten restrictions even more. Even as reformers made progress, however, courts began to sign off on government evasions of debt limits. As a consequence, such limits “have had only a modest effect on aggregate state and local debt,” writes Columbia Law School’s Richard Briffault. Judges, he notes, “appear to share with state governors and legislators a belief in the legitimacy of the modern activist state.” In the words of the New York State Court of Appeals, judges have often proved open to any “modern ingenuity, even gimmickry” that legislators can cook up to get around debt restrictions.

Today, states and localities engineer most of their borrowing through what Briffault calls “non-debt debt,” a term for bonds designed to avoid legal restrictions on borrowing. For example, courts in some states have decided that when a state’s independent authorities issue bonds, that borrowing isn’t restricted by constitutional debt limits—even if taxpayers are ultimately on the hook for it. If a legislature takes on debt itself, that also doesn’t count against constitutional restrictions on borrowing, according to the judiciaries in some states. Briffault estimates that such evasions are responsible for three-quarters of state debt and two-thirds of municipal obligations incurred through bond offerings. The growth of this kind of borrowing helps explain why state and local debt outstanding from municipal securities has blasted from $2 trillion (in today’s dollars) in 2000 to nearly $3 trillion today—real growth of 50 percent in little over a decade.

New York State has turned to court-sanctioned gimmickry again and again. Though New York’s constitution requires that voters approve any new government debt, only 5 percent of the state’s $63 billion in outstanding borrowing has received voter authorization, down from 10 percent a decade ago. Meantime, the cost of servicing that debt has risen by an average of 9.4 percent annually. Partly because of such unsanctioned borrowing, New Yorkers bear the nation’s second-highest per-capita load of state debt, says New York’s comptroller. The state is still paying off what it owes from the infamous 1991 Attica prison deal, in which New York, trying to close a budget deficit, “sold” the facility to one of its independent authorities, which borrowed the money to pay for it. New York also still counts on its books debt from the 1970s bailout of New York City, which, thanks to refinancing, it won’t pay off until 2033.

Other New York deals engineered without voter say-so include a $2.7 billion bond offering in 2003, backed by 25 years’ worth of revenues from the state’s gigantic settlement with tobacco companies. To circumvent borrowing limits, the state created an independent corporation to issue the bonds and then used the money from the bond sale to close a budget deficit—instantly consuming most of the tobacco settlement, which now had to be used to pay off the debt. Legislators engineer such borrowing because they aren’t confident that voters would agree to new debt: of the seven bond offerings that Empire State voters have considered over the past 25 years, four went down to defeat.

Thanks to its low state debt, Texas enjoys a reputation for budgetary restraint. Yet as Texas comptroller Susan Combs found to her dismay, the state’s towns, cities, counties, and school districts have racked up the second-highest per-capita local debt in the nation, behind only New York’s spendthrift municipalities. The total, nearly $8,000 per resident, is more than seven times higher than Texas’s per-capita state debt. Over the last decade, local debt in the Lone Star State has more than doubled, growing at twice the rate of inflation plus population growth. At the moment, Texas localities owe $63 billion for education funding—155 percent more than they did a decade ago, though student enrollment and inflation during that period grew less than one-third as quickly. The borrowing has also paid for a host of expensive new athletic facilities, such as a $60 million high school football stadium, complete with video scoreboard, in the Dallas suburb of Allen.

As in Cook County, so many different levels of government in Texas can issue debt that taxpayers, bewildered by the complexity of it all, let overlapping districts keep on borrowing. As an example, Combs describes how the residents of a single Houston block must repay debt incurred by the county, the city, the city’s school district, and Houston Community College, among other entities. “I went to dozens of town hall meetings around the state, and when I asked, not a single member of the public knew just how much people in their towns were on the hook for,” she says.

Texas, like New York, amassed all this debt by pushing the limits of the law. Though taxpayers must approve most government borrowing, Texas provides an exception for localities that need to issue debt quickly: a “certificate of obligation,” borrowing that doesn’t require approval unless 5 percent or more of local voters petition to have a say on it (a rare occurrence, since most don’t even know that they have that power). Since 2005, Texas localities have issued nearly $13 billion worth of these certificates, often for dubious ends. In 2010, for instance, Fort Worth borrowed nearly $35 million through certificates of obligation to build a facility for horse shows.

Texas school districts have made use of another controversial financing technique: capital appreciation bonds. Used to finance construction, these bonds defer interest payments, often for decades. The extension saves the borrower from spending on repayment right now, but it burdens a future generation with significantly higher costs. Some capital appreciation bonds wind up costing a municipality ten times what it originally borrowed. From 2007 through 2011 alone, research by the Texas legislature shows, the state’s municipalities and school districts issued 700 of these bonds, raising $2.3 billion—but with a price tag of $23 billion in future interest payments. To build new schools, one fast-growing school district, Leander, has accumulated $773 million in outstanding debt through capital appreciation bonds.

Capital appreciation bonds have also ignited controversy in California, where school districts facing stagnant tax revenues and higher costs have used them to borrow money without any immediate budget impact. One school district in San Diego County, Poway Unified, won voter approval to borrow $100 million by promising that the move wouldn’t raise local taxes. To live up to that promise, Poway used bonds that postponed interest payments for 20 years. But future Poway residents will be paying off the debt—nearly $1 billion, all told—until 2051. After revelations that a handful of other districts were also using capital appreciation bonds, the California legislature outlawed them earlier this year. Other states, including Texas, are considering similar bans.

Judges have proved especially eager to approve evasions of debt limits when they’re the ones demanding that states or localities spend money. Back in 2001, New Jersey’s activist supreme court mandated that the legislature embark on a project of building and refurbishing schools (see “The Court That Broke Jersey,” Winter 2012). To comply, Trenton lawmakers announced a plan to borrow $8.6 billion through a bond offering—a shockingly high sum. Taxpayer groups reacted with such outrage that officials knew that voters would never endorse the move. So the legislature decided to channel the borrowing through an independent authority. The taxpayer groups sued, but the state supreme court brushed their objections aside, arguing that a clear precedent existed for such borrowing. The state quickly burned through half of the borrowed money on patronage and inefficient construction practices, so it borrowed another $3.9 billion, again through the authority. Taxpayers, needless to say, will foot the bill.

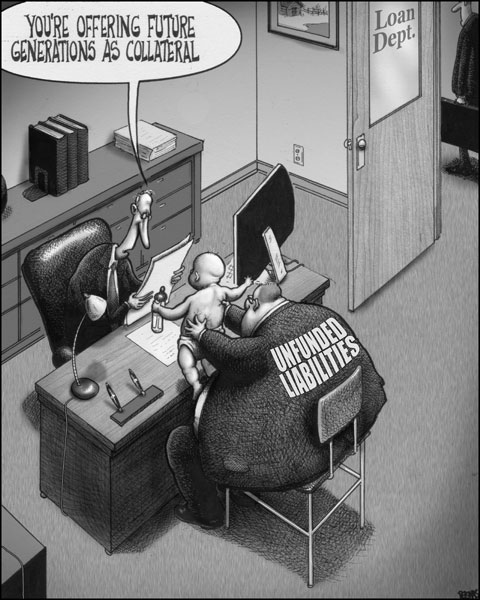

If you define municipal debt simply as what states and localities have borrowed, the total nationwide comes to about $3 trillion. Nevertheless, these governments actually owe more than twice that much, according to estimates from groups like the States Project. The reason for the discrepancy is that states and localities carry another kind of debt—promises of retirement benefits to public-sector workers—and they have radically underfunded the systems that must pay for it. As Boston University Law School professor Jack Michael Beermann wrote recently in the Washington and Lee Law Review, the situation is a “double whammy” for future taxpayers, who not only will have to pay for “the consumption of prior generations” but also will receive “reduced government services” as increased spending on retirement debt crowds out other programs.

Some states have laws stating that annual funding of future pension or health-care payments must be considered part of current budgets, but as Beermann points out, many states don’t. Those states can therefore run deficits—even if they have balanced-budget requirements, as most do—by shortchanging retirement accounts. A report by the Pew Center on the States showed 29 states failing to make the necessary payments into their pension systems in 2010, the latest year for which data are available. Over the last decade, Kansas, a prime offender, has contributed less than 80 percent of the necessary dollars to fund employee pensions, according to a recent report by the Kansas Policy Institute. Even in an economically robust year like 2006, the state government managed to set aside just 64 percent of the necessary funds, one reason that Kansas’s state pension system is less than 50 percent funded.

State and local governments have likewise made ambitious promises to finance the health care of their employees when they retire, yet they have set aside almost no money to do it. Instead, they’re purchasing the health care on a pay-as-you-go basis as workers retire. With workers quitting earlier and living longer, governments suddenly find themselves with little room in current budgets and zero reserve funds. State governments owed nearly $700 billion in health-care promises to retirees, the Pew study estimated, but they had set aside only about 5 percent of that amount. The study found that only one state, Alaska, had paid in advance for more than 50 percent of its obligations. Even states with low levels of other debt had done little to finance retirees’ health-care benefits; Texas, for instance, had set aside just 1 percent of the funds. Similarly, a Pew study of 61 big American cities determined that they owed $126 billion in health-care promises and had paid for only 6 percent.

Consider Michigan, where crushing government retirement costs helped push Detroit into insolvency, leading to a state takeover of the city’s fiscal management. With Detroit’s debt crisis in view, Governor Rick Snyder commissioned a study of the level of health benefits promised retirees throughout Michigan. The study, the first of its kind, concluded that the state’s municipalities had put aside, on average, just 6 percent of what was necessary to finance their retirees’ health care; the remainder, some $12.7 billion, hadn’t been funded. The city of Lansing, for example, already devoted $20 million of its $150 million annual budget to retirees’ health care, the study observed; yet its unfunded liabilities were so great that to fund the debt properly each year, it would have to double property-tax rates. Many municipalities, the study added, had done little to control debt. More than half required no annual contribution from government workers to help fund their future health-care costs.

Earlier this year, a commission created by Chicago mayor Rahm Emanuel reported that that city’s health-care costs for retirees would rise from $109 million in the 2013 budget to $541 million in a decade. Chicago has since decided to drop its current health-insurance program and shift all retirees onto the health-insurance exchange being set up in Illinois under President Obama’s Affordable Care Act. That insurance will be cheaper because the federal government will subsidize the rates of the exchanges, basically getting taxpayers nationwide to pick up some of the cost for Chicago workers.

In some places, elected officials have promised benefits to workers without even a cursory effort to calculate what they might add up to. Before the California city of Stockton filed for bankruptcy last year, auditors listed “uncontrolled pension, health, and other benefit cost increases” as a big part of the city’s woes, including a whopping $400 million unfunded liability for retirees’ health care. “No one gave a thought to how it was going to eventually be paid for,” said a financial manager brought in to address the fiscal difficulties.

Stockton may be an extreme example, but after its bankruptcy, officials in other California municipalities began asking what their cities owed. Earlier this year, to take one example, Sacramento officials commissioned a study to measure their city’s debt. In what the Sacramento Bee reported as a “sobering” city council session, the city manager explained that Sacramento had racked up some $2 billion in obligations—a “big and scary” number, the manager said, for a city of 477,000 residents with an annual general-fund budget of just $366 million. Nearly half of that debt was retirement-related, including $440 million for retirees’ health care. To pay down the debt, the city estimated, it would have to put aside $43 million annually, or 12 percent of the general fund. City officials added that it wouldn’t be easy to solve the problem by firing workers, since Sacramento had already cut some 1,200 employees, or 20 percent of its workforce, in the last several years.

Estimates of state and municipal debt have been growing for another reason: more and more independent experts are exposing local governments’ faulty accounting standards. The Chicago-based Institute for Truth in Accounting observes that governments are balancing their budgets using “antiquated budgeting rules and accounting standards,” adding that “hundreds of billions of dollars of unfunded retirement systems’ liabilities are not reported on the face of states’ balance sheets.”

One problem, the group says, is that half of all states don’t bother to file their required annual financial reports on time. Local governments are guilty, too. Though the Securities and Exchange Commission (SEC) requires any government that issues municipal bonds to file a Comprehensive Annual Financial Report, a 2011 study by the California Debt and Investment Advisory Commission estimated that one in four Golden State local governments in that position failed to file the report on time—and one in ten never filed it at all, even though the SEC gives states and cities three times as long to file as it gives private companies. In May, the SEC cited Harrisburg, Pennsylvania, for failing to file reports for two years, even as the city collapsed into insolvency.

Another source of dispute involves the way states and cities calculate pension debt. For starters, they often use a nineteenth-century form of balance-sheet math known as cash-basis budgeting, in which you don’t report expenses until they’re paid. This approach lets local governments ignore costs, such as retirement obligations, that are building up today but aren’t payable for years to come.

Also, the loose accounting standards that states and cities use, recommended by the Governmental Accounting Standards Board, allows them to calculate pension debt using their own projected annual rate of return on the investments that they make, rather than a rate set by an independent body or by some preestablished formula. The higher the projected returns, the lower the pension debt appears to be; unsurprisingly, the projections tend to run high. The rules governing private pensions in the United States, as well as both private and government pension systems in Europe and Canada, are much more restrictive. Economists Aleksandar Andonov, Rob Bauer, and Martijn Cremers noted in a recent paper that corporate pensions in the United States, as well as private and government pension systems in Canada and Western Europe, had significantly lowered their investment projections as interest rates declined, reasoning correctly that lower rates made it harder to hit lofty investment goals. By contrast, government pension funds in the United States responded to lower interest rates by increasing risky investments and maintaining high projections of market returns (see “The Pension Fund That Ate California,” Winter 2013). In the United States, government funds projected gains of 8 percent, on average, the study found; government funds in Canada and in Europe projected returns of 6.7 percent and 3.6 percent, respectively, considering those targets more realistic.

Different projected returns can result in significantly different debt calculations. In 2011, the nonpartisan Congressional Budget Office pointed out that, according to states’ own accounting methods, their pension systems had $700 billion in unfunded debt. But if you used a lower, more plausible, rate of return, the CBO added, total unfunded pension debt was somewhere between $2 trillion and $3 trillion—and the amount has kept growing since then.

Some states have intentionally used the complexity of pension accounting to mislead taxpayers and investors. Over the last three years, the SEC has accused two states, New Jersey and Illinois, of making deceptive and fraudulent statements to potential investors about the health of their employee-pension funds. The SEC said that Illinois failed to tell investors both that its plan to bail out its troubled pension system wouldn’t actually achieve that goal and that the system was “structurally underfunded,” meaning that without further reform, it would fall still deeper into debt. Illinois also failed to report that it used a form of pension accounting that funds a larger percentage of an employee’s retirement costs near the end of his career, increasing the system’s risk of running out of money. In New Jersey’s case, the SEC disclosed that the state had neglected to tell investors that it wasn’t adhering to a financing plan that it had concocted to stabilize its pension system, creating a “fiscal illusion” that it could meet its financial requirements.

Eventually, such soft accounting slams into reality, and pension systems begin to miss investment projections. Governments then find themselves contributing more and more each year to keep the system afloat. New York City’s average pension contributions have risen from 6.1 percent of its budget in 2005 to 11.5 percent today, according to a recent paper by Manhattan Institute scholar Daniel DiSalvo. In 2005, pension payments consumed 43 percent of income-tax revenue; in 2013, “every penny in personal income tax we collect will go to cover our pension bill,” Mayor Michael Bloomberg recently complained. America’s second-largest city, Los Angeles, has seen its pension payments rise from 3 percent of its budget to 18 percent today. Atlanta’s pension payments increased from $43 million annually in 2002 to $144 million in 2010, consuming 19 percent of its budget, before the city finally initiated pension reforms that capped costs and began reducing debt.

Even as governments scramble to find ways of paying their existing obligations, taxpayers should demand fundamental reforms that will make state and local leaders more fiscally responsible going forward. An easy place to start would be a push for honest accounting and greater transparency. States and cities need to move away from cash-basis budgeting and adopt the accrual accounting that private corporations and the federal government use, in which future expenses are included in current reckonings, providing a clearer picture of long-term debt.

Taxpayers should also demand that states and cities produce timely financial reports. The SEC should slap governments and elected officials with harsher penalties for failing to file on time or at all. To date, the commission has mostly just required states to agree not to miss future deadlines. And reformers should strive to make state balanced-budget amendments rigorous again. Some states that have recently enacted pension reform, such as New Jersey, have written into law that the government must make its required annual pension contributions: a budget wouldn’t be considered “balanced” if officials ignored that requirement.

At the same time, states need to remove some of the discretion that retirement systems have to calculate pension obligations, including their discretion to predict future investment returns. Handing that task to an independent body or determining it with a formula—perhaps one linked to the movement of interest rates—would remove some of the political manipulation of retirement accounting. The ratings agency Moody’s and the Governmental Accounting Standards Board have each proposed new, more accurate, ways of calculating pension debt. But these new standards will have little effect unless states and cities respond to them by contributing more to their pension systems or by cutting benefits.

An even better way to make retirement plans more honest would be to replace defined-benefit plans with hybrid systems, as some states and cities have already done. Such systems start with a 401(k)-style defined-contribution plan featuring individual retirement accounts and then add either Social Security (in places where public workers receive it) or, in lieu of Social Security, a basic, inexpensive defined-benefit plan that pays a small monthly pension. Taxpayer obligations to workers are much clearer in defined-contribution plans, since the government must simply contribute a certain percentage of a worker’s salary into an account each year, eliminating the vexed question of whether it can afford to pay a defined pension many years down the road.

Reformers should also seek to get rid of the many loopholes that state legislators use to get around debt-limit rules. In particular, states should be banned from assuming debt through independent authorities or by direct appropriation of the legislature. Reform should also cap state-supported debt by tying it to some flexible measure of economic or revenue growth, such as state personal income, rather than just stating a dollar limit.

Reformers should strive, too, to end governments’ use of debt to balance budgets, perhaps by introducing a requirement that all taxpayer-supported debt be used for capital projects, such as schools, roads, and bridges. Such structures endure for decades, so it’s reasonable to ask future residents to contribute to their construction through debt payments. By contrast, bonds floated to close a particular year’s budget, pledging to the bondholders that they’ll be paid with future lottery, toll, or tobacco revenues, give today’s residents a benefit at future residents’ expense.

There’s no single cure for the debt crisis afflicting state and local governments. But unless taxpayers start pulling harder in that everlasting tug-of-war, they can expect to keep losing ground.