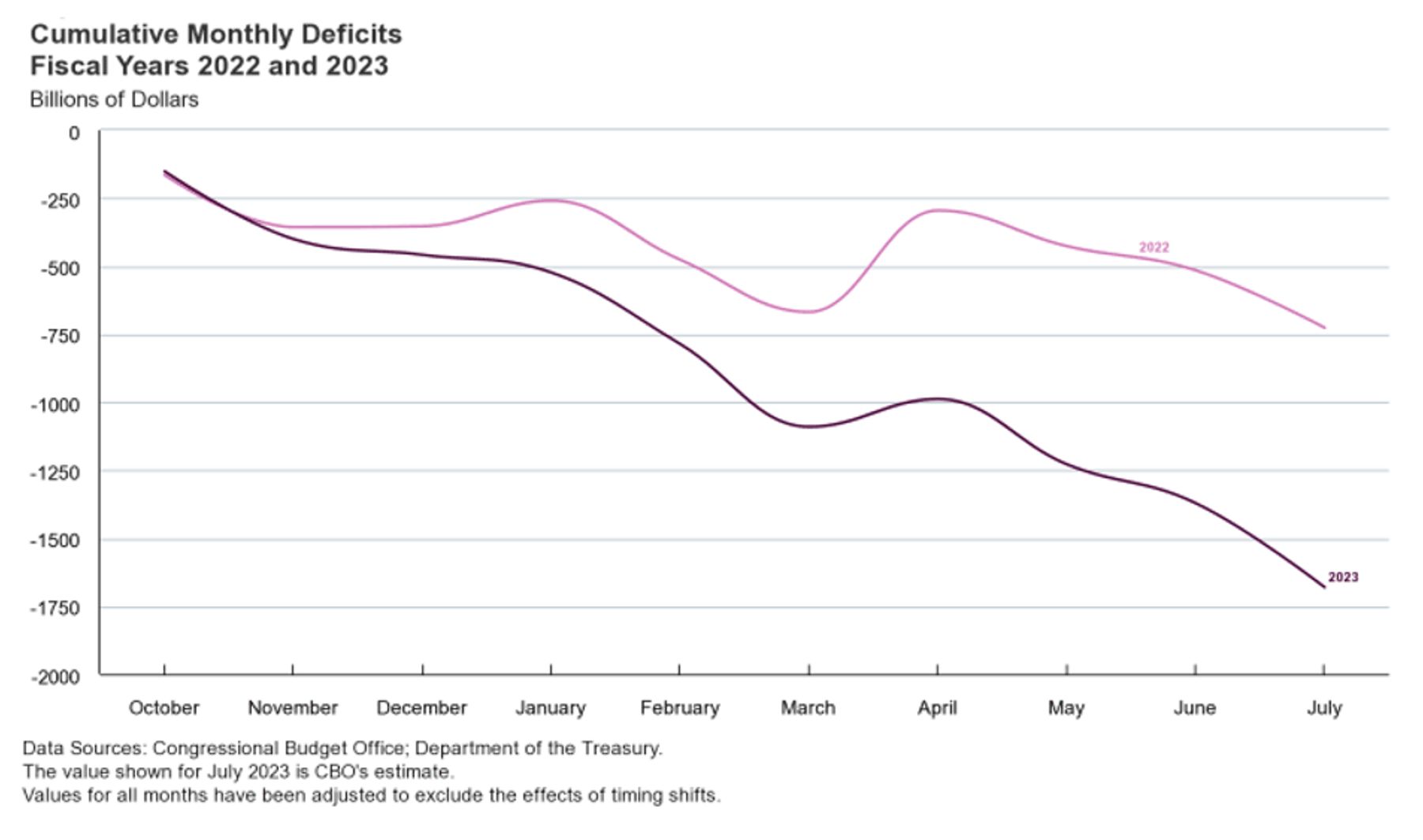

In its latest monthly budget review, the Congressional Budget Office documented that the federal budget deficit in the first ten months of fiscal year 2023, clocking in at $1.6 trillion, was more than twice the shortfall during the same period in 2022. This enormous fiscal expansion has occurred even though the Biden administration’s massive pro-cyclical fiscal stimulus packages were passed in 2021 and 2022.

The extra deficit comes from both a 10 percent fall in revenues and a 10 percent hike in spending. Each figure is the product of many factors. Explanations for the revenue decline include lower capital gains taxes (2022 was a bad year for the stock market); lower average effective tax rates (brackets were ratcheted up steeply last year but much less so this year); delays to filing deadlines in California and Georgia until October, due to weather; and lower remittances from the Federal Reserve to the Treasury, as its interest-rate hikes have swung the Fed from a net earner to a net loser on its assets and liabilities. In total, the CBO now expects revenues for the year as a whole to run $400 billion less than previously projected.

Finally, a reason to check your email.

Sign up for our free newsletter today.

Meantime, spending is up largely because of massive hikes in entitlement costs, driven in part by cost-of-living adjustments for inflation. Another cause of spending increases is the interest burden from servicing the national debt, which has already widened the deficit by almost $150 billion. But while those spending increases are automatic adjustments mandated by law, other increases are not. For instance, the Biden administration expanded the definition of sport utility vehicles to include luxury sedans so that more cars would qualify for the expanded electric vehicle tax credits introduced by the highly inflationary Inflation Reduction Act (IRA).

By playing language games to ensure that even $80,000 luxury sedans qualify for $7,500 taxpayer-funded credits, the administration dramatically raised the expected cost of the IRA, funneling more cash into the economy than legislators had originally intended. So no one should be surprised if we continue to see deficits come in above expectations in the future. While the CBO initially expected the IRA’s environmental provisions to cost less than $300 billion, forecasters have upped their estimates, and some independent analysts now expect that the IRA’s tax credits alone could end up costing $780 billion, almost three times the original projection.

A deficit of 6.3 percent of GDP during peacetime—and when inflation risks remain present and economic output is above potential—is irresponsible in both the long and short term. As the recent Fitch downgrade of U.S. debt highlights, America’s long-term fiscal path is becoming less and less tenable. By the middle of the century, the majority of tax revenue collected will be needed to finance interest payments to bondholders, unless we raise tax rates to levels that will cripple the economy. The Trustees of the Social Security and Medicare trust funds expect them to run out of money in 2033 and 2031, respectively, requiring significant tax hikes to pay their expected obligations.

In the shorter term, the Fed’s record-smashing monetary-tightening cycle is bound to hit the economy sooner or later. When it does, the economy is likely to enter recession. The deficit will grow even larger, since recessions reduce revenues via lower income bases and increase outlays via automatic stabilizers like unemployment insurance.

If we enter a recession beginning with a deficit over 6 percent of GDP and federal debt owned by the public near 100 percent of GDP and those levels increase from there, two relevant consequences will follow. First, the government’s ability to use countercyclical fiscal policy to blunt the pain of the recession will be much more limited, as there will be less fiscal space available. Second, markets may be less eager to embrace the safety of U.S. Treasury bonds. Usually, a recession generates a “flight to safety” response in financial markets that lowers Treasury yields, providing some stimulus to the economy. If that response is more muted than usual because of the enormous supply pressures driven by profligate borrowing, then lower yields may have less ability to cushion the falling economy.

Moreover, lingering inflation pressures from the 2021–22 experiments in monetary and fiscal policy adventurism may limit the Fed’s ability to cut interest rates to offset recessionary weakness in the labor market. In an average recession, the Fed cuts interest rates by about 5 percent. Due to recent memories of high inflation, the Fed might be able to deliver only a portion of an average cutting cycle, limiting its ability to offset economic weakness.

Therefore, we will be meeting any future economic downturn with our hands partially tied behind our backs, unable to use our strongest fiscal and monetary policies to ameliorate job losses. That’s why running a pro-cyclical fiscal and monetary policy—which stimulates borrowing even as the economy booms above its potential—is such a terrible idea. Good times are for prudent policy and saving up bullets for when things get dangerous. As it turns out, we might not have any bullets left when we need them. Congress should start cutting fiscal spending immediately, so that the country can return to a stabler and saner policy mix.

Photo: matthiashaas/iStock