In the middle of the Mojave Desert, just off Interstate 15 between Los Angeles and Las Vegas, sits the Mountain Pass mine. Surrounded by a high plateau of pale rock and desert scrub, this 600-foot-deep open pit hums with activity. Trucks haul blasted rock to the surface, where it is crushed in pursuit of valuable minerals that are scattered thinly through the earth’s crust yet remain indispensable to modern life.

Buried within the rocks of Mountain Pass are rare-earth elements—a group of metals that play a vital role in nearly every twenty-first-century technology. They help make the high-strength magnets that power electric vehicle motors, the phosphors that light up television screens, the guidance systems inside precision missiles, and the tiny speakers and vibration motors in smartphones. The elements have become so critical that the U.S. government now calls them “essential for national security and economic resilience.”

Finally, a reason to check your email.

Sign up for our free newsletter today.

Despite their importance, however, Mountain Pass is the only rare-earth mine operating in the United States. Nearly all the world’s rare earths are mined and refined elsewhere—mostly in China, which, over the past several decades, has built an industrial empire around the extraction and processing of these materials. China now accounts for about 70 percent of global rare-earth mining and over 90 percent of the refining and magnet production.

That wasn’t always the case. When the Mountain Pass mine opened in 1952, it quickly became the world’s leading source of rare earths, supplying materials for everything from color televisions to the earliest computers. Well into the 1980s, the mine continued to produce the majority of global rare-earth output. But as environmental regulations tightened and costs rose in the U.S., China began dominating the market through a mix of cheap labor, lax standards, and aggressive industrial policy. By the early 2000s, the Mountain Pass mine had shuttered. China controlled nearly the entire supply chain.

That reliance on Beijing is increasingly uncomfortable for Washington and for the industries that depend on these materials. Mountain Pass eventually reopened in 2018 and now produces roughly 47,000 metric tons of rare earths annually—just over 10 percent of global supply. Some initial refining occurs on-site, but most of the material still gets shipped to China for final processing before being sold to manufacturers around the world.

The stakes have only risen. In April, China retaliated to a round of U.S. tariffs by restricting exports of seven rare-earth elements to the United States. In October, Beijing took an even more extreme measure, threatening to curb trade of any minerals or products that contain even trace amounts of those elements. The move rattled supply chains and exposed a hard truth: the world’s most technologically advanced nation now depends on its largest geopolitical rival for the materials that make its most important technologies work.

Uncomfortable questions now confront U.S. policy. How did America lose control of these materials? Can it rebuild its capacity in time? And if it does, can it do so without sacrificing its market dynamism or succumbing to the kind of state-directed industrial policy that too often stifles innovation?

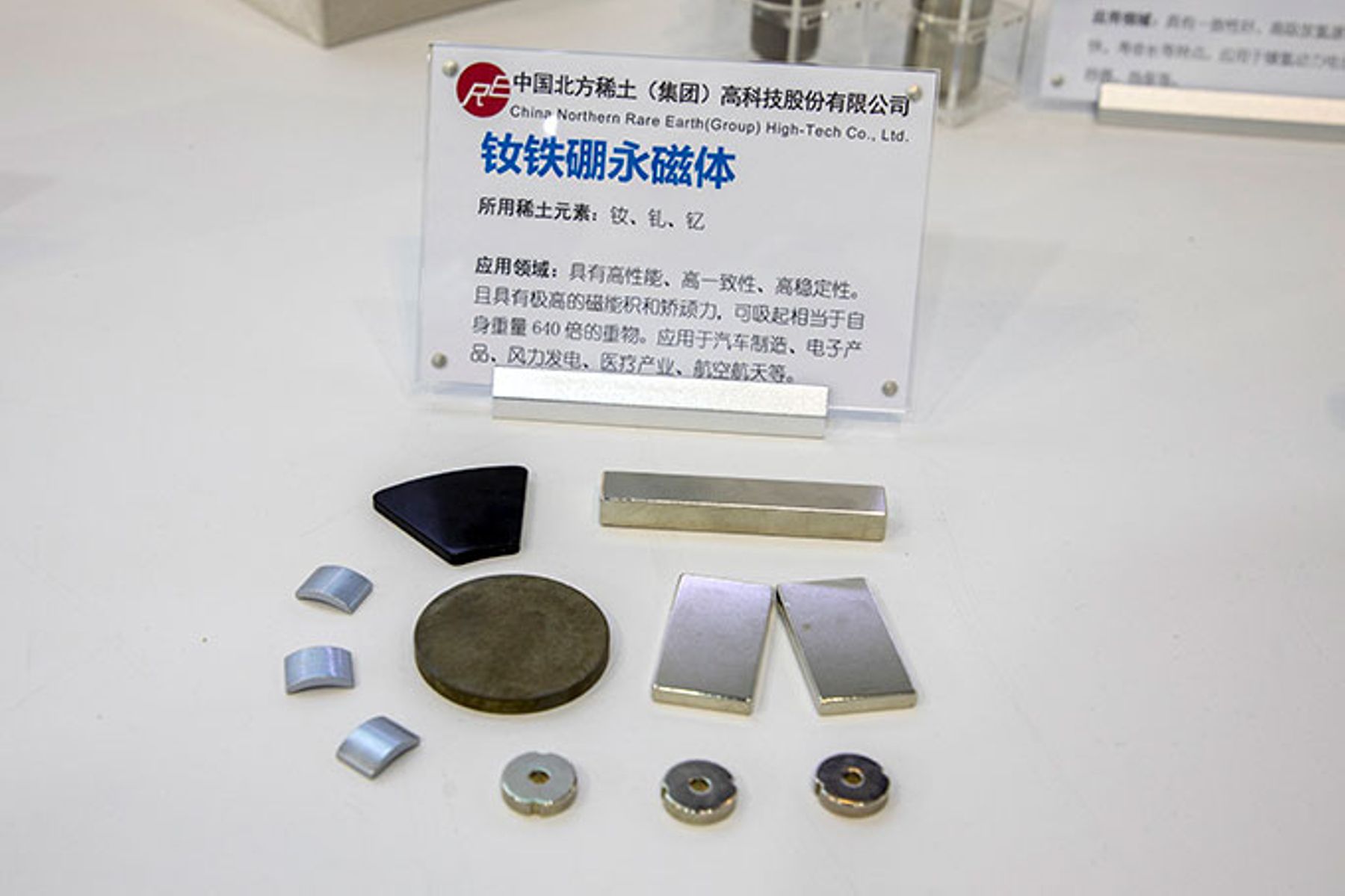

Rare earths are a group of 17 metallic elements found in small concentrations throughout the earth’s crust. Despite the name, they’re not especially rare; they just don’t occur in forms easy to mine or separate. The elements often cluster with other minerals, making them difficult to process. Refining these trace metals—with obscure names like dysprosium, praseodymium, and xenotime—into usable materials requires a long chain of complex chemical and thermal steps.

Most people would be hard-pressed to name a single one; but once refined, these elements serve as the hidden infrastructure of modern life. Without them, many of the world’s most advanced machines and everyday conveniences simply wouldn’t work as designed. The magnets that they form are the strongest and lightest in the world, allowing electric motors, precision drones, and household appliances to operate with quiet precision and exceptional efficiency. Europium gives color to television and computer screens. Neodymium powers the magnets inside smartphones, hard drives, and electric motors. Gadolinium enables MRIs. Cerium helps refine oil and polish glass. Lanthanum sharpens camera lenses and night-vision optics. Ytterbium drives fiber-optic cables and wireless transmitters. Dysprosium is used in nuclear-reactor control rods. Yttrium is essential for the manufacturing equipment that produces the advanced semiconductors powering NVIDIA and other chipmakers.

And rare earths like these are especially important for modern defense technologies. They make possible radar, sonar, guidance, and other critical military communications systems. They power the actuators that steer missiles, the sensors that guide aircraft, and the motors that keep drones in the air. A single F-35 fighter jet contains nearly 1,000 pounds of rare-earth materials embedded in its engines, flight-control systems, and sensors. An Arleigh Burke–class destroyer warship contains nearly 6,000 pounds. A Virginia-class submarine needs 10,000.

Rare earths belong to a larger family of critical minerals, including lithium, nickel, cobalt, and graphite, that underpin everything from batteries and semiconductors to satellites and renewable energy systems. Mining these materials often carries a significant environmental toll. Yet together, they are as vital to the twenty-first century as steel and oil were to the twentieth. Unlike oil, however, they are controlled very little by America.

The irony is that the emergence of renewable energy and other green technologies in the United States has made mining these materials more important. Electric vehicles require six times more mineral input than a conventional car. A single wind turbine contains hundreds of pounds of rare-earth magnets. According to the International Energy Agency, global demand for critical minerals could double by 2030, driven largely by increased electricity demand. The new economy is not postindustrial; it’s just built on a different kind of mining.

China sits at the center of this emerging global supply chain. Over the past four decades, it has built an industrial ecosystem that dominates every step of rare-earth production, from mining and chemical separation to metal refining and magnet manufacturing. It now produces nearly all the world’s high-performance rare-earth magnets.

That dominance didn’t happen by accident. Beginning in the 1980s, Chinese leaders saw a strategic opportunity. In 1992, former Chinese leader Deng Xiaoping famously declared that “the Middle East has oil; China has rare earths.” His government backed the sector with cheap loans, loose environmental rules, and direct investment, driving costs so low that foreign competitors often could not survive. While firms elsewhere closed mines and shuttered processing plants, China’s rare-earth industry scaled up as it developed expertise across the entire mine-to-magnet supply chain.

Meantime, America threw up green roadblocks to opening new mines or processing facilities. Laws such as the National Environmental Policy Act and the Clean Water Act made the permitting system increasingly burdensome. Compliance costs soared. Projects became entangled in red tape, often devolving into decade-long ordeals. In the name of protecting the environment, the United States effectively outsourced its mining—and its pollution—elsewhere.

By the late twentieth century, mineral extraction had come to symbolize environmental harm. A generation of policymakers, investors, and activists viewed extractive industries as backward and incompatible with progress. Federal laws prioritized preservation over production. “Not in my backyard” became national policy.

Reversing that decline is no simple matter. Opening a mine in America can require years of environmental reviews and permitting battles. One recent analysis found that the U.S. has the second-longest mine-development timeline in the world, lasting nearly 29 years from discovery to production, on average. Only Zambia takes longer. And the whole process is highly uncertain, for even when a project gains approval, litigation can further delay or derail projects. Environmental groups and other antidevelopment interests exploit procedural requirements in environmental laws as a pretext for impeding development. These challenges add years—and millions of dollars in costs—to projects, and if a court sides with the plaintiffs, agencies often have to restart the entire review process from scratch.

Examples abound. A proposed copper mine in Arizona was recently blocked after 14 years of investment and environmental review, undone by an obscure dispute over the validity of mining claims under an 1872 federal law. In Alaska, environmentalists continue to fight a road that would provide access to mineral-rich deposits of copper, cobalt, and rare earths, holding up permits for years through protracted litigation. And in Nevada, two lithium projects have faced a series of regulatory and legal obstacles, including a dispute over whether one of the mines will affect a nearby species of rare desert buckwheat.

And mining is only half the equation: the expertise and infrastructure required to refine and separate rare earths have largely migrated overseas. Today, ore, whether mined in the U.S., Australia, or elsewhere, is typically sent to China for final refining before being sold into the global market, giving Beijing significant leverage. By controlling the refining and magnet-making stages, China doesn’t just supply most of the world with rare earths; it dominates nearly every aspect of the market.

China has shown a growing willingness to exploit that control, especially in response to U.S. trade policy. In recent years, Beijing has taken steps to restrict exports of specialized equipment used to process rare earths and even barred some Chinese citizens with expertise in rare-earth materials from traveling abroad. And over the past 12 months, China has significantly tightened its controls.

After the Trump administration imposed steep reciprocal tariffs on Chinese imports earlier this year, Beijing retaliated by imposing strict export rules on seven rare-earth materials, as well as the magnets made with them. The metals could no longer be exported without a special license from China. The restrictions caused some automakers in the U.S., Europe, and Japan to delay production. Then, in October, ahead of high-stakes trade talks with Trump, Beijing went even further—announcing export-license requirements for more rare-earth elements and for any products that contain more than 0.1 percent of them. To approve these, applicants would need to submit exhaustive technical data on product designs and supply-chain plans, effectively forcing companies to reveal proprietary details to Beijing. Given the country’s rare-earth dominance, such rules would have effectively given China veto power over vast segments of global trade and manufacturing.

In response, Trump threatened to impose a new 100 percent tariff on imports from China, as well as other export controls of its own. The standoff rattled markets and alarmed manufacturers that depend on rare-earth materials. When Trump and Chairman Xi Jinping finally met in late October, the two sides agreed to pause the confrontation. China would delay its new export rules for a year in exchange for a partial rollback of U.S. tariffs. The underlying dispute over rare-earth leverage and tariffs, however, remains fully intact.

The conflict revealed the extent to which the U.S. government is willing to go to counter Beijing’s rare-earth industrial policies. After China’s initial threat, the U.S. responded by taking the extraordinary step of purchasing equity stakes in several private companies in the critical-mineral sector, including MP Materials, which operates the Mountain Pass mine in California. In July, the Pentagon became the company’s largest shareholder—through a $400 million investment yielding a 15 percent stake—and set a 10-year price-floor guarantee for its materials in order to ensure continued production.

Similar deals soon followed. In October, the Department of War acquired a 10 percent stake in Trilogy Metals, a Vancouver-based company exploring for copper, cobalt, and several rare earths in Alaska. The Department of Energy took a 5 percent stake in Lithium Americas, which is developing a massive lithium mine and processing facility at Thacker Pass, Nevada. Other deals are reportedly in the works, as well as an effort to build a “strategic mineral reserve” to stockpile key materials.

The United States has also sought to deepen partnerships abroad. In October, it signed a new agreement with Australia to boost joint investment in rare earths and critical minerals. The two countries pledged investments of over $3 billion in mining and processing projects over the next six months. As part of the agreement, the Pentagon announced plans to help finance construction of an advanced gallium refinery in Australia. “About a year from now,” Trump said at the signing ceremony, “we’ll have so much critical mineral and rare earths, you won’t know what to do with them.”

These arrangements signal a new era of industrial policy for Washington. Beyond just supporting allies in the production of select minerals of strategic national security importance, Washington is taking a page out of China’s playbook by taking partial ownership of key industries—something more common in, say, Europe. U.S. officials have stressed that most of these equity stakes are not meant to be permanent. Nonetheless, they mark a profound shift in U.S. economic policy and set an uneasy precedent for future government intervention.

China’s decision to flex its rare-earth dominance was, in many ways, a predictable reaction to America’s own protectionist turn. The Trump administration’s tariff hikes invited retaliation, and Beijing struck back where it held undisputed leverage. The deeper irony lies in what followed: Beijing’s move pushed Washington into copying its playbook. What began as an effort to counter China’s state-directed industrial strategy has led Washington to drift in the same direction—marked by subsidies, price guarantees, and government equity stakes in private firms.

The result is an industrial policy arms race, with each government claiming to defend its markets by distorting them further. In trying to free itself from dependence on China, the United States has taken steps toward the state capitalism that it once opposed.

China’s dominance in rare earths gives it leverage but not absolute power. Each time Beijing tries to use its position for strategic advantage, it strengthens the incentive for others to find ways around it. “The problem for Beijing is that the more it rolls out the big guns of export restrictions on critical minerals, the more it encourages the Western world to bite the bullet and build alternative supply chains,” commodities expert Clyde Russell recently wrote. “China doesn’t even have to fire the cannon, the repeated threat of doing so will be enough to spark the necessary Western investment.” In that sense, Beijing’s latest moves may prove self-defeating, accelerating the very diversification that it seeks to avoid.

History offers a preview. When China abruptly halted rare-earth exports to Japan in 2010 after a maritime dispute, it shocked Japan’s manufacturers, who relied heavily on Chinese supply. Though the ban lasted just two months, it encouraged Japan to change its approach. Tokyo began investing heavily in non-Chinese rare-earth mining projects, in addition to promoting stockpiling, recycling, and alternative technologies. Japan’s dependence on Chinese rare earths has since declined significantly—from 90 percent to 60 percent today—and its total consumption of rare earths is now half of what it was 15 years ago. Beijing’s attempt to exert pressure ultimately eroded its own influence.

A similar response may already be under way. In Wyoming, plans are solidifying for what could become the first new U.S. rare-earth mine in more than 70 years. Other exploration projects are moving forward across North America and Australia. In June, the European Union announced plans to support rare-earth projects in South Africa and Malawi. Significant untapped reserves of rare earths can also be found in Brazil, India, Vietnam, and Greenland.

Investments in refining capacity are advancing. Last summer, MP Materials announced an expansion of its efforts to build two domestic rare-earth magnet-manufacturing plants, with support from the War Department. These facilities would allow the company to process and refine ore from its Mountain Pass mine, giving the United States its first mine-to-magnet supply chain. Once fully operational, the plants could become the largest producer of neodymium-based magnets outside of China.

A search for substitutes is ongoing, as researchers and manufacturers seek to develop technologies that rely less—or not at all—on rare earths. Minneapolis-based Niron Magnetics, for example, is working to develop rare-earth-free permanent magnets using iron nitride that could eventually replace neodymium. Automakers such as Tesla and Audi are deploying induction motors that require no rare earths at all, while BMW and Renault are producing models with rare-earth-free synchronous motors that use wound rotors instead of permanent magnets.

Much of this adjustment can, and should, happen through market forces and private initiative. Where policy can play a constructive role is in making adaptation easier.

The most obvious starting point is permitting reform. Streamlining environmental review and permitting processes for mining projects would make domestic production more viable without sacrificing environmental safeguards. Projects that meet clear environmental standards should face predictable, transparent timelines instead of endless procedural hurdles. In March 2025, Trump signed an executive order to accelerate domestic mineral production, which invoked emergency powers to fast-track permits and unlock federal lands for critical mineral projects, including rare earths.

Legal reform is equally important. Timelines for judicial review, deadlines for court decisions, and limits on protracted litigation could help break the so-called litigation doom loop that often drains capital and saps private investment in domestic mining. The SPEED Act, cosponsored by Representatives Bruce Westerman and Jared Golden and advanced by the House Natural Resources Committee in November, would amend the National Environmental Policy Act to do just that. Such reforms would benefit U.S. national security, but they have an environmental justification, too: more mining activity would shift from unregulated regions to the U.S., where property rights, transparency, and environmental protections are stronger overall.

Beyond permitting, strategic partnerships can help diversify supply. The U.S. and Australia joint effort to invest in rare-earth and critical-mineral projects could be expanded to other allies. In recent months, Washington has already inked similar deals with Japan, Thailand, and Malaysia.

Some targeted government support may be necessary as well, particularly for defense applications where rare-earth substitutes are limited. Fighter jets, missiles, and radar systems require materials that can perform under extreme conditions where rare-earth alternatives remain inadequate. Treasury Secretary Scott Bessent has recently floated a “Warp Speed” initiative for rare-earth processing, modeled on the pandemic-era vaccine program, to accelerate investment in this narrow domain. Stockpiling critical minerals for national security, as the United States has long done with oil, may also make sense.

Even so, such interventions should be approached with caution. A modest reduction in dependence on China could be enough to supply the most critical uses without resorting to permanent subsidies or market-distorting state ownership. As rare-earth analyst David Merriman recently told The Economist, the West could “significantly derisk” its position by reducing its reliance on China from 90 percent of consumption to 60 or 70 percent—a level sufficient to meet its most essential needs. The point is not to mine and refine every gram of rare earths that we consume but to ensure that our supply is diversified and competitive enough that no single nation can credibly threaten a cutoff.

For that reason, Washington should resist the urge to create an open-ended rare-earth industrial policy that entrenches government ownership and control over private industry. In a world of rapid technological change, there’s a risk that today’s rare-earth anxiety could become tomorrow’s sprawling network of subsidies and state-backed enterprises chasing yesterday’s strategic priority.

China’s grip on rare earths endures only so long as it keeps them cheap, abundant, and apolitical. Ultimately, the best way to counteract China’s monopoly is not to mimic it but to outgrow it—through competition, innovation, and the confidence that markets, if allowed to work, can do what command economies cannot.

The task for Washington is not to replace rare-earth markets, then, but to create the conditions for markets to adapt to, and end, Chinese domination. Policymakers should intervene only narrowly, otherwise letting competition drive adaptation. The government can help by reforming permitting laws and providing clear incentives for private investment. It would hurt by entrenching itself as a long-term operator in America’s private sector.

China’s rare-earth monopoly is already showing its limits. Its control of the market lasts only so long as it keeps the minerals flowing freely. The more China uses supply as leverage, the faster others will develop alternative supplies or substitutes. America’s response should reflect that reality—not by mirroring Beijing’s central planning but by cultivating the dynamism and ingenuity that have always been America’s greatest resource.

Top Photo: The Mountain Pass mine in the Mojave Desert, the only rare-earth mine operating in the United States (Timothy Swope/Alamy Stock Photo)