New York City, dependent on Wall Street for a quarter-century, has gotten used to harsh cyclical economic downturns, including the lending contraction in the early nineties and the bursting technology bubble in 2000. But today’s turmoil may be not a cyclical downturn for Wall Street but instead the beginning of an era of sharply lower profits as it rethinks its entire business model. If so, it will produce the biggest economic adjustment and fiscal challenge that New York has confronted in more than three decades. If the city’s leaders don’t recognize this challenge and move quickly to meet it, New York could soon face an acute fiscal crisis rivaling its near-bankruptcy in the mid-seventies.

Such a fate—almost unthinkable to a city that has grown complacent about its world-class standing—could set Gotham back in the colossal strides that it has made over the past two decades in restoring its citizens’ quality of life. As Mayor Michael Bloomberg said in May, we must “pray that Wall Street does well.” But we’d better have a plan if it doesn’t.

Finally, a reason to check your email.

Sign up for our free newsletter today.

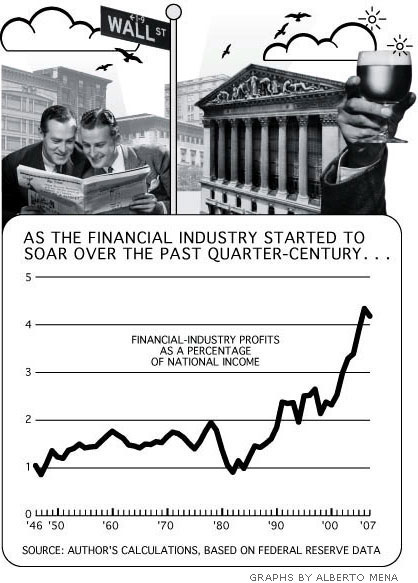

Wall Street bankrolled New York’s long recovery from the seventies because New York, through its long economic, fiscal, and social deterioration, managed to keep its position as the nation’s financial capital just as finance was about to take off. In the early eighties, the nation’s financial industry—particularly Wall Street—was feeling its way toward a sweet spot where it would stay for two decades. As Federal Reserve chief Paul Volcker brought inflation under control, creating a stable environment for financial innovation and a stable currency for the world’s savings, baby boomers and international investors flocked to U.S. markets. The Dow Jones Industrial Average tripled between 1982 and 1990, despite the ’87 crash, while the assets of securities brokers and dealers more than doubled as a share of America’s financial assets. The financial industry also saw a huge opportunity in Americans’ increasing love of debt, creatively packaging it into everything from mortgage-backed securities to junk bonds and then selling it to investors. Between the early 1980s and the early 1990s, the financial sector’s profits as a percentage of the nation’s income more than doubled. The sector’s pretax income as a percentage of all national income started a similar march upward. Profits at securities firms, while choppy, easily doubled between the early eighties and the end of the decade (all numbers are inflation-adjusted unless indicated otherwise).

New York reaped massive rewards from Wall Street’s good fortune. The city’s financial-industry employment grew by 14 percent in the eighties—more than triple the job growth in its other private-sector industries. Jobs in the securities industry in particular, which had decreased in the seventies, grew by more than a third. Since these positions were high-paying, they had an outsize impact: by the late eighties, according to the

Fed, financial services contributed nearly 23 percent of New Yorkers’ wages and salaries, up more than 60 percent from the previous decade. And financiers’ heavy spending supported other jobs, from restaurant workers and interior decorators to teachers and nurses.

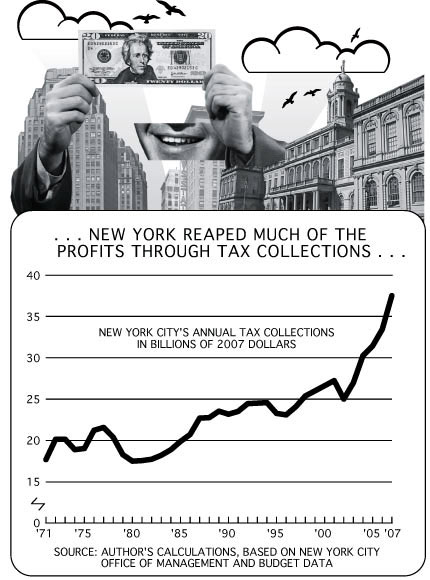

For evidence of how Wall Street started to lure newcomers to New York, look to Hollywood. Movies chronicling Gotham’s grim decline, like Taxi Driver (1976) and Escape from New York (1981), gave way to films portraying the heady excitement of making millions in the city, like Wall Street (1987) and Working Girl (1988). While much of the city remained grimy and dangerous, the excitement outweighed those factors for young, child-free baby boomers who paid high taxes without requiring many city services. The result: after hemorrhaging nearly 10 percent of its population between 1970 and 1980, New York gained nearly 4 percent back between 1980 and 1990. The city’s tax take in 1981 had been slightly lower than its take a decade before; but by 1991, it was raking in a third more than in 1981.

This money allowed New York to reverse some of its bone-scraping seventies-era budget cuts and to invest in infrastructure without making the politically difficult choice of cutting deeply into social services. In the seventies, the city had laid off nearly 3,000 police officers and 1,500 sanitation workers; in 1985, Mayor Ed Koch hired 5,300 cops and almost 1,000 sanitation workers. In the 1990s, it was largely Wall Street’s breakaway success that gave Mayor Rudy Giuliani the financial resources to focus on making New York City safe again.

If high finance found its sweet spot in the eighties, it reached dizzying sugar highs starting in the late nineties and continuing, after recovering from the tech bust and 9/11, until last year. The nation was awash in the world’s money, encouraging record lending and speculation as well as the creation of more financial products, which yielded banks massive profits. By 2006, the financial industry’s corporate profits as a percentage of the nation’s income had doubled once again.

It seemed that nothing could go wrong for Wall Street once it had bounced back from the tech bubble’s burst. With the dollar serving as the expanding global economy’s reserve currency, banks had oodles of money to lend. Cheap Asian imports were keeping prices and inflation expectations low, allowing central bankers to justify low interest rates. Beginning in the nineties, traditional consumer banks—previously tightly regulated to protect government guarantees for their depositors—began taking investment risks that once had been confined to Wall Street. As time went on, investment banks became more dependent on fees from debt backed by home mortgages and other consumer products, further blurring traditional lines between investment and consumer banking.

The financial world took advantage of the easy money and better technology. It booked high fees by designing ever more complicated “structured finance” products, backed by riskier home mortgages as well as corporate loans. Wall Street sold these products to international investors, who couldn’t get enough of American debt, by making a seductive pitch: the products were structured so intricately that even risky mortgages were as safe as government bonds, and they paid better interest rates. Further, if an investor ever had to sell a mortgage-backed security after he had purchased it from a bank, it was a cinch, since Wall Street had “securitized” individual loans—that is, taken thousands of them at a time, sliced them up, and turned them into easily tradable bonds of different risk levels.

In addition to lending, Wall Street was borrowing at record levels so that it could take bigger and bigger risks with its shareholders’ money, making up for lower profit margins on businesses like equity underwriting and merger advisories. Wall Street’s borrowing as a multiple of its shareholders’ equity was 60 percent above its long-term average by the end of last year (with sharp increases over the past few years). Firms were taking even more risks than that figure indicates, setting up arcane, off-the-books “investment vehicles” with shareholders still vulnerable if something went wrong.

As banks and financiers got unimaginably rich, so did the city. The finance industry’s contribution to New Yorkers’ wages and salaries topped out at over 35 percent two years ago. Last year, the city took in 41 percent more in taxes than it did in 2000, capping off an era of unprecedented revenue growth. While the city’s stratospheric property market—itself a function of Wall Street bonuses and easy money—drove much of that increase through property-related taxes, corporate tax revenues rose by 52 percent, personal income tax revenues by nearly 20 percent, and banking tax revenues by nearly 200 percent.

But today, the financial industry may be entering a wilderness period of lower profits, employment, and bonuses. “Whether it’s financials as a share of the stock market or financials as a share of GDP, we’ve peaked,” ISI Group analyst Tom Gallagher told the Wall Street Journal in April. One measure of how this downturn differs from those in the recent past: some Wall Street firms, after their disastrous miscalculations, are operating today only because the Fed, as Bear Stearns melted down in March, decided to start lending to investment banks, which it doesn’t normally regulate or protect.

A new alignment of global demographics, inflation expectations, and interest rates may spell long-term trouble for the city’s premier industry. A decade ago, cheap Asian goods kept prices and inflation expectations down; today, Asia’s growth is pushing them up. Ballooning energy prices and too-low interest rates threaten to yield sustained inflation. America now faces intense competition—particularly from the euro—for the world’s savings and investment, meaning that it can’t depend on attracting as large a portion of the world’s nest egg to keep interest rates down. “It is not credible that the world will revert to the same level of capital flow to the U.S. after the credit crunch is over,” Jerome Booth, research head of U.K.-based Ashmore Investment Management, noted recently. The Fed can keep official rates low only at the risk of inflation and more capital flight. The end of cheap money means that the market for future debt may shrink, squeezed by tougher borrowing terms, cutting off a crucial profit line for banks.

Regulators, too, will be harder on the banks. Because investment banks now benefit from taxpayer-guaranteed debt, taxpayers must be protected. The feds probably won’t let firms borrow from private lenders at the levels that they have over the past decade, and it’s unlikely that they’ll let banks rely so intensely on short-term debt—which is cheaper, but riskier, than long-term debt. (Short-term lenders can flee quickly, as the Bear Stearns crash showed, because they have the option of yanking their money out of investments, often overnight, while long-term lenders are stuck with the bets that they’ve made.) Less borrowing means lower profits, and not just temporarily. Regulation might also curtail Wall Street’s lucrative business of complex derivatives, another huge area of risk. Plus, international stock listings continue to bypass New York for Asia and Europe because of the six-year-old Sarbanes-Oxley law, which imposes an unnecessary regulatory burden on companies publicly traded in the U.S., and also because the world’s growth has moved east. Such losses could be ignored only when debt and derivatives were making up for it.

The skepticism of Wall Street’s own investors and clients, though, is the real deal-breaker. The most startling news out of the current crisis is that Merrill Lynch, UBS, and others didn’t know that they had taken certain risks for shareholders, lenders, and clients until they were already reporting tens of billions in losses. Clients and investors shouldn’t mind losses when they understand the risks that they’re taking. They do mind if, after the firm that they’re investing in or doing business with has insisted that its careful models and safeguards protect them, it turns out that its only protection from bankruptcy is Uncle Sam.

International investors will not again blindly trust Wall Street’s ability to assess and allocate risk. “Market participants now seem to be questioning the financial architecture itself,” Fed governor Kevin Warsh said recently. Don’t forget the stock market’s performance, either: it hasn’t been impressive over the past eight years.

New York City, so dependent on the financial industry’s continued growth, should shudder.

If Mayor Bloomberg and his successor view the current downturn as another short blip, rather than a long readjustment of the financial industry’s share of the economy, and they turn out to be wrong, the decisions that they make could prove ruinous. Over the past two and a half decades, whenever the financial industry underwent one of its periodic downturns, New York stuck to the same playbook: jack up taxes to make up for lower tax revenues, cut spending a bit, and wait for the financial industry to come roaring back. During the early nineties’ credit crunch, Mayor David Dinkins slapped two temporary surcharges on the income tax; one still persists. In 2002 and 2003, after the tech bust and 9/11, Bloomberg temporarily hiked income and sales taxes and permanently hiked the property tax.

Those tax increases were never wise because they kept less profitable industries and their lower-paid employees out, making New York ever more dependent on finance. Even the financial industry didn’t ignore the tax hikes; partly in response, it sent back-office, five-figure-a-year jobs to cheaper cities, and as a result, New York today has less than one-fourth of the nation’s securities-industry jobs, down from one-third two decades ago. Still, the industry was growing so fast that it and its workers could withstand the higher costs posed by the tax increases.

But what was once merely unwise could be calamitous today. Consider the last time that New York tried raising taxes when its premier industry was about to shrink—the mid-sixties, when the city’s leaders arrogantly believed that its record population of 7.9 million people, in the middle of a record economic boom, wouldn’t mind paying for a breathtaking array of Great Society social programs, as well as fattened public-employee benefits. In 1965, the New York Times had reminded city leaders that “New York City’s economy is prospering,” and its editorialists decreed a year later that “strong medicine, specifically higher taxes, is the remedy for restoring New York’s financial health.”

Mayor John Lindsay, with state support, enacted the city’s first personal income taxes, as well as new business taxes, in 1966. New York went on to lose half of its 1 million manufacturing jobs between 1965 and 1975—a trauma as great as Wall Street’s troubles today, because in 1960, manufacturing had accounted for more than a quarter of New York’s jobs. At the same time, the city was also losing its collection of corporate headquarters and their legions of well-paid employees. By the end of the seventies, half of its 140 Fortune 500 companies had fled the city.

New York didn’t anticipate this change or understand its significance as it was happening. Well into the early seventies, the city thought that it could keep taxing and spending because the future was bound to mirror the “Soaring Sixties.” City officials argued that fleeing companies were evidence of New York’s success because some companies just couldn’t afford to be here any longer. Worse, the city’s leaders didn’t understand how quickly urban quality of life could deteriorate: as they focused on social spending rather than vital public services like policing, murders shot up from 645 in 1965 to 1,146 just five years later. Nor did they realize how quickly middle-class residents would flee, taking their tax dollars with them.

For a while, the city and its lenders found a way around these miscalculations. New York stepped up its borrowing against future tax revenue in the late sixties and early seventies, paying the banks back when the following year’s tax receipts rolled in. The foolishness of such a plan was always obvious: three years before the city skirted bankruptcy, the Times reported, Albany skeptics warned that large-scale temporary borrowing was folly. But even as economic and fiscal conditions worsened, the city kept spending and spending. In 1970, city leaders were heartened by the judgment of bond-rating agency Dun & Bradstreet, which noted New York’s “extraordinary economic strength . . . and long-range credit stability.” (Then, as now, ratings agencies weren’t good at predicting acute crises.) In 1972, as what had once seemed like a short downturn stretched on, Times editorialists encouraged complacency, noting that “after all the years of . . . warnings of imminent municipal bankruptcy, it is reassuring to find investors . . . bullish about the outlook for New York City’s long-term financial soundness.”

By late 1974, however, as rising spending outpaced tax receipts, a crisis was inevitable. It came the following spring, when New York wrestled with a budget deficit that equaled 14 percent of its expected spending and creditors cut the city off. Forced to throw itself at the mercy of the state and federal governments for emergency funding, Gotham gutted trash pickup and policing, murders climbed to 1,500 annually, and more residents left.

Millennial New York likes to think of itself as vastly superior to the troubled city of the 1970s. But once again, on the brink of what may be a major economic upheaval—this time, involving the financial sector rather than manufacturing—it is reacting with disturbing complacency. And yet again, the mayor has allowed the budget to swell dangerously during the good times, which could push leaders to make the same mistakes as were made in the sixties and seventies: raising taxes at precisely the wrong time and slashing vital services under pressure to keep up social and public-employee spending.

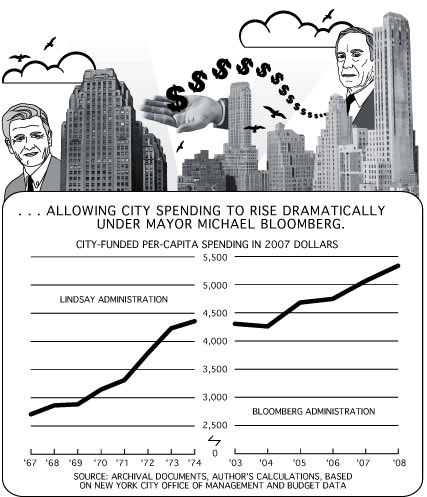

During the past decade, New York used the cash that Wall Street was showering on the city not to ease its long-term problems but to make them worse. In 1974, under Lindsay, the city devoted one-quarter of its budget to social spending: welfare, health services, and charities. Today, the city continues to spend one-quarter of its budget on social services (not including the public schools’ vast social-services component). Nor has New York reformed the pensions and size of its still-huge public workforce, reduced debt costs, or cut Medicaid costs fueled by Albany’s powerful medical lobby, which helps ensure that New York’s per-capita Medicaid spending—rife with waste and fraud—is the highest in the nation. Even after adjusting for inflation and considerable population recovery, the city’s tax-funded budget for 2008 is 22 percent higher than it was at its Lindsay-era peak. While spending rose just 9 percent or so during the Giuliani era, it has risen three times as fast since—the highest rate since Lindsay left office.

Echoing a time when people said that New York was ungovernable, Mayor Bloomberg often calls these costs “uncontrollable.” But there was no better time to start controlling them than during the past half-decade, an era of unparalleled prosperity and public safety when Bloomberg had an opportunity available to no other modern mayor. If he had successfully bargained with Albany and union employees to require new workers to contribute more to their pensions and health benefits, we would have seen the results by now. Likewise, if he had worked with Albany to rein in Medicaid spending—now nearly $6 billion a year—the city could have spent some of that money to build schools and fix roads, reducing debt costs. Instead, we’ve got a politically powerful public workforce that commands benefits belonging to another era and that remains vulnerable to corruption despite this generosity, as recent construction investigations show.

The mayor has also sharply increased spending in one area that was easily controllable: the city’s public schools budget, up by more than one-third since 2001 even though enrollment is down 4 percent. Much of that spending funds plusher teachers’ salaries and the higher pensions that follow, plus borrowing costs for school construction and rehab, making it harder to cut than it was to increase. Today, the education budget is nearly $21 billion: one-third of the entire budget, and more than police, fire, and sanitation combined.

Bloomberg’s failure to control costs during the boom means that big trouble looms. The city projects that spending over the next three years will increase by more than 20 percent, while revenues will increase by just 13 percent (neither figure is adjusted for inflation). If that happens, a $5 billion–plus deficit—more than 11 percent of tax-funded spending—will result in two years’ time. Moreover, that’s the best-case scenario, based on the city comptroller’s prediction of low growth this year and next and a quick, though weak, recovery after that. But the mayor expects a 7.5 percent economic contraction this year, followed by a smaller contraction. If that happens, revenues might not rise as much as 13 percent; in fact, they might shrink, as they often did in the seventies (and again in 1990 and 2002).

This risk is especially acute because our progressive tax structure and the growth in wealth of our richest citizens over the past two decades make New York highly dependent on the rich, whose income is volatile. Two years ago, the top 1 percent of taxpayers paid nearly 48 percent of the city’s personal income taxes even after adjusting for the temporarily higher tax rate, up from 46 percent in 2000, 41 percent a decade ago, and 34 percent two decades ago, according to economist Michael Jacobs at the city’s independent budget office. A few bad years for the city’s wealthiest translate into a few terrible years for their home base.

Cutting a $5 billion deficit—let alone an even larger one—is a formidable task even when done slowly. Cutting such a deficit in a hurry two years from now, under an inexperienced mayor, will endanger the city’s vitality. It’s not too late for Bloomberg to prepare the budget for a painful economic adjustment, and not just by cutting around the edges of the “controllable” budget, as he’s prudently done this year and last.

The first principle is to do no harm on the tax side. Bloomberg will allow a temporary property-tax cut to expire, and he has told the Times: “If all else fails, we’re not going to walk away from providing services, and only then would I think about a tax increase, and my hope is that we’ll avoid it.” He’ll have to: while the city has proved that it can squeeze higher taxes out of a phenomenal growth industry, that trick won’t work on an industry that’s stagnant or in decline. New York’s sky-high income taxes for businesses and residents already put the city at a huge disadvantage, since they keep away lower-paying jobs from media, technology, and other industries that otherwise might be attracted by lower housing costs and commercial rents in the coming years. The city can’t afford to make this disadvantage any worse.

Second, the mayor must carefully manage his budget cuts. This year, he proposed largely across-the-board cuts of about 6 percent in projected spending, covering everything from police and sanitation to homeless services and education. He also enacted a 20 percent slash to the long-term capital budget, which funds physical infrastructure. But this strategy won’t work for long. Vital services can’t withstand deep cuts. The mayor must not alienate the middle class, whose tax revenues he needs, and that means protecting the police department, cleaning streets, and keeping libraries open. (His May delay in hiring 1,000 new police officers for more than a year, even as New Yorkers are becoming wary of crime again, is worrisome.) Further, failing to fix decaying infrastructure isn’t a way to save money. It’s no different from borrowing to pay for other expenses, since waiting will worsen deterioration and mean more expenses later.

So as Bloomberg readies his final budget over the next year, he’ll have to choose the deepest cuts to projected spending carefully, even though it requires fighting the city council, which nixed half his proposed cuts this year and especially protected education. Rising education spending under both Bloomberg and Giuliani hasn’t improved scores on national tests, after all. And within the capital budget, the city should reduce its spending on economic-development and affordable-housing subsidies in order to fund things like roads and transit adequately. Furthermore, New York pols should stop regarding the operating and capital budgets as unrelated. Ten percent of Medicaid’s $6 billion annual take would go a long way toward upgrading the city’s roads and subways. Last, tens of millions of dollars in politically connected earmarks by both the mayor and the council are unsavory in good times and unconscionable in bad.

But ultimately, the mayor can’t fix the city’s budget without addressing its “uncontrollable” half, whose growth will be responsible for three-fourths of the deficit in three years’ time. Bloomberg—and his successor—can use fiscal stress to advantage in bargaining for changes in city contracts. In the past, in fact, the city’s biggest bargaining gains have come during fiscal turmoil. As Charles Brecher and Raymond D. Horton noted in their 1993 book, Power Failure: New York City Politics and Policy Since 1960, the city won sanitation productivity gains in 1981, while it was suffering the fallout from the fiscal crisis of the 1970s, and a less costly pension tier two years later. While police officers won a raise this year that was necessary to attract recruits, the mayor must not let the city’s other unions bring home similar gains through contract renegotiation.

The city’s contract with more than 100,000 non-uniformed workers expired this spring, presenting an opportunity. New York should negotiate to get this union, DC-37, to allow new employees to accept a pension plan in which the city contributes to workers’ private accounts, rather than guarantees a pension for life. The independent budget office estimates sizable budget savings here—nearly $100 million annually—within half a decade. Requiring health-insurance-premium payments of 10 percent from these workers and retirees would save half a billion dollars more; extending the workweek from 35 and 37 hours to 40 (imagine!) would net another half-billion, savings that the next administration will dearly need if Wall Street doesn’t roar back. The mayor (and his potential successors) must impress upon unions that their members won’t get a better deal if they wait.

But why the urgency? After all, New York has huge advantages today. Half a century ago, suburban growth was driven by cheap fuel, fast commutes, and low crime. Today, suburbs are choked off by congestion, $5-a-gallon gas, and bad public schools. The city’s governance approach is also different. If crime starts to rise, we know what to do: aggressively police neighborhoods and prosecute and sentence defendants appropriately. And the city’s new citizens—many of whom have invested their lives’ savings in their homes—should help politicians keep some focus, counterbalancing to some extent the organized pressure to sacrifice all else for education spending. The city’s budget has safety latches, too. New York’s fiscal near-death in the seventies spurred the state to impose extraordinary oversight and brought about local changes. The city can’t borrow much today for operating spending. It must balance its budget annually and project four years’ worth of expected spending and revenues, submitting the results to a state board.

Yet these advantages aren’t limitless, as recent high-profile shootings in Harlem and Far Rockaway indicate. If a mayor lets crime spiral out of control over a crucial one- or two-year period, it will be harder to control later. The middle class won’t be patient for long if its voice isn’t heard, and the city’s “global” upper class is much more transient than it was 40 years ago. Plus, with one-third of the population leaving every decade, New York must continually attract new residents. As for city finances: no amount of regulation can guard against complacency. The city couldn’t have balanced its budget this year and reduced next year’s deficit if not for the huge surplus that Wall Street provided last year, before it ran out of steam. The city doesn’t have to default on its bonds to get into trouble, as it nearly did three decades ago, moreover. Sacrificing quality of life so that it can pay those bonds would do as much damage. Finally, if the city does need help, it can’t look to New York State to bail it out, as it did 33 years ago: this time around, Albany might be in equally dire straits.

Even if we do all the hard work of fixing the budget and in two years’ time, Wall Street is defiantly humming along, once more channeling record tax revenues into the city’s coffers, the steps that we take today won’t have been wasted. By acting now, Bloomberg will enable his successor to consider income tax cuts and infrastructure investment. Just as we prepare for a terrorist attack that we hope will never come, we have to prepare for a fiscal and economic crisis that we hope will never come. The risk is real.