The financial-market implosion and the coming transformation of the securities industry will expose the fundamental flaw in New York State’s woefully overextended public finance model. The state budget is today geared to run on an ever-expanding stream of high-octane revenues from a Wall Street that no longer exists—and the rest of New York’s economy isn’t nearly robust enough to make up the difference.

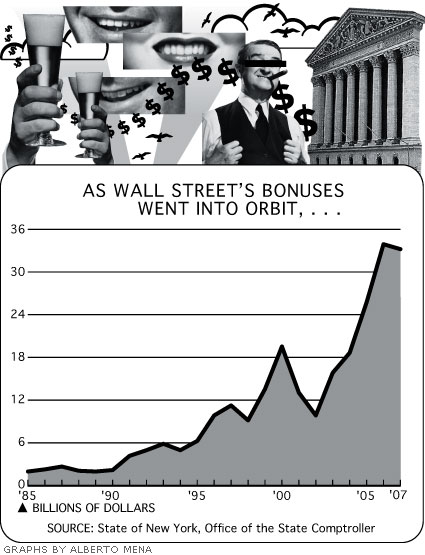

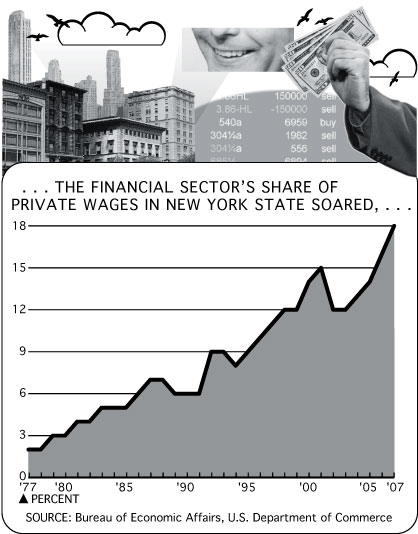

With an occasional bear-market interruption, the state’s financial dependence on Wall Street has grown steadily for more than a quarter-century. As New York’s once-mighty manufacturing sector shriveled, the securities industry’s share of all private wages in the state more than quadrupled, growing from 3 percent to 14 percent between 1980 and 2000. And after the 2000–02 downturn, Wall Street’s share of the state revenue base took another giant leap. By 2007, securities-industry wages and bonuses in New York had climbed to nearly 18 percent of private-sector wages in the state (compared with just 2 percent in the rest of the country). The average Wall Street salary and bonus as of last year was a staggering $379,000—more than six times the average for all private-sector jobs in the state.

Finally, a reason to check your email.

Sign up for our free newsletter today.

Handsome wages translate into sizable taxes. Wall Street bonuses and salaries probably accounted for at least one-third of the net increase in state income tax liability between 2002 and 2007. That’s not counting the (taxable) capital gains and dividends generated by the last stock-market boom, or the (taxable) profits that investment banks, private equity firms, and hedge funds generated for other New York businesses, from black-car companies to white-shoe law firms. Last year, New York State’s 212,000 securities-industry employees generated more income taxes for Albany than did the 3 million or so households reporting incomes below $50,000.

In fact, while the securities industry accounted for less than 3 percent of New York’s employment and 9 percent of its GDP last year, Wall Street generated 20 percent of state tax revenues. Since the financial sector’s bonus babies made so much to start with, their pay hikes were fully taxed at the marginal state income tax rate of 6.85 percent. And the income tax is imposed on all wages and salaries earned in New York, including by residents of other states—effectively exporting a portion of the tax burden to New Jersey and Connecticut. The state thus has an even more immediate and direct fiscal stake in Wall Street than does New York City, where the economic impact of the crisis is potentially much broader and deeper.

And now all those numbers have gone shuddering into reverse. At best, New York State will experience a repeat of fiscal years 2000–01 through 2002–03, when income tax revenues dropped 16 percent, with the decrease concentrated entirely among upper-income households. At worst, a broader, more serious national recession will push New York into a much deeper hole.

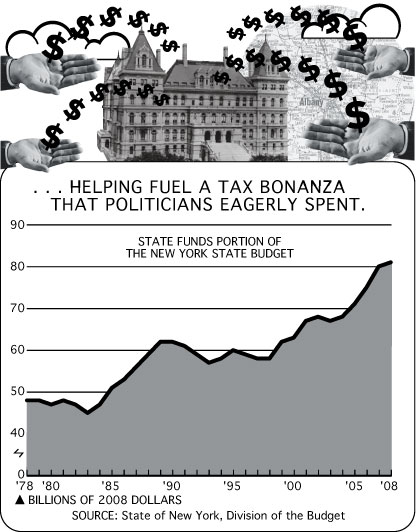

The financial crisis will take the blame for New York’s looming budget crunch, of course. But the fundamental problem is out-of-control government spending. During Republican George Pataki’s third and final term as governor, which ended in 2006, the “state funds” portion of the budget (the part that excludes federal aid) rose 19 percent when adjusted for inflation, including billions added by the state legislature over Pataki’s vetoes. The rate of spending growth was the fastest since Democrat Mario Cuomo’s second term in the late 1980s—which, not by coincidence, provoked the state’s worst fiscal crisis since the 1970s. Yet this time around, Wall Street churned up so much new revenue that Pataki could leave behind a $3 billion cash balance. That rapidly shrinking cushion is now all that keeps New York from sinking into a deep pool of red ink.

In January 2007, Democrat Eliot Spitzer became the first New York governor since Franklin Roosevelt to take office just as the economy was peaking—giving him plenty of room to engineer a soft landing before it was too late. But after campaigning on a pledge to control spending, Spitzer only made things worse. His first budget called for an 8 percent spending hike (which, he absurdly countered, represented “spending control” because it was lower than the 11 percent increase enacted by the legislature during Pataki’s last year).

Worse still, Spitzer built his budget around a proposed $7 billion, four-year increase in the largest category of state spending: school aid. This was a striking departure from the budget-control strategies adopted by his predecessors in both parties. Because school finance (unlike Medicaid) is almost entirely shaped by state law and because legislators perennially treat education as their Number One budget priority, Pataki, Cuomo, and Democratic governor Hugh Carey all understood the necessity of holding down school aid in their executive budget proposals (and did so except when running for reelection themselves). They would then grudgingly allow the legislature to “buy” increases in school aid, sometimes in exchange for other budget concessions. Spitzer and his staff derided this process as a childish charade. But it served its purpose.

Predictably, the legislature sweetened Spitzer’s new formula before adopting it. But pouring so much new money into what was already the nation’s best-funded public school system only encouraged school districts across the state—including New York City’s—to expand programs further, hire additional staff, and fatten already generous teachers’ contracts. At the same time, putting yet more pressure on the budget, Spitzer and the legislature agreed to a four-year, $2 billion expansion of Pataki’s huge STAR program, which gave state-subsidized school-property-tax breaks to suburban and upstate homeowners (and further relieved pressure on school districts to constrain spending).

In his second budget, released last January, Spitzer proposed another spending increase, this time of 6 percent, despite clear signs of big trouble brewing in the financial sector. Negotiations with the legislature had barely begun when his dalliances with prostitutes forced him to resign—the same week, coincidentally, that Bear Stearns collapsed.

The Public-Sector House of Cards

As the U.S. financial markets froze, two front-page New York Times stories about how retirees were faring made a jarring contrast. One, on September 23, painted the picture you’d expect of worried seniors squeezed between eroding 401(k)s and skyrocketing property taxes on homes they believed safely bought and paid for. The other, two days earlier, reported that almost every recent retiree from the taxpayer-subsidized Metropolitan Transportation Authority’s Long Island Rail Road division had successfully claimed disability benefits from a special federal fund for railway workers after they had retired, so that former train engineers still in their fifties were raking in up to $170,000 a year. Their purported disabilities entitle them to free use of state recreation facilities: a mordant page-one photo showed a youthful and healthy-looking taxpayer-supported LIRR retiree enjoying a complimentary round of golf on a taxpayer-owned Long Island course.

This rip-off, which the state attorney general is investigating, is an almost comically extreme case of a scandal now so widespread that we hardly notice it: public-sector employees living better than the private-sector workers who struggle to pay the ever-rising taxes that support their supposed servants. The average public-sector worker’s wages are more than a third higher than his private-sector counterpart’s, as Steven Malanga reported in these pages (“The Conspiracy Against the Taxpayers,” Autumn 2005), and with fringe benefits like health care and retirement thrown in, his total compensation swells to almost half again as great as the private-sector average. Unlike most private-sector workers, whose 401(k) retirement plans shift all risk to them, public-sector workers have guaranteed pensions, which kick in earlier and are much richer than the few remaining defined-benefit private-sector pensions, and they boast automatic cost-of-living hikes to boot.

Economist Herb Stein famously remarked, “Anything that can’t go on, won’t.” The current credit mess is one spectacular case in point: when Congress pushes banks to give mortgages to borrowers of doubtful creditworthiness, when banks find they love doing so, when outfits like Fannie Mae package the loans into bags of a lot of nothing that together supposedly add up to something, and when million-dollar-a-year thirtysomething Wall Street quants claim to have a formula for putting an exact dollar value on that something, the whole house of cards is bound to collapse. Another case in point is the public sector’s house of cards. Since public-employee unions, along with government-subsidized social-services and health-care outfits, have become the new powerhouses of our city and state politics, elected officials, dependent on their financial and campaigning support, have gladly showered other people’s money upon them, especially for pensions, which won’t have to be paid out until the pols are only names on some pork-barrel stadium or hockey rink. One by one, businesses and individuals (like today’s hard-pressed private-sector retirees) decide they won’t or can’t pay the taxes, and they leave. The collapse comes in slow motion, but inexorably: once-legendary cities—Baltimore, Buffalo, Detroit, Philadelphia—fade into ghosts of their former greatness.

New York has escaped that fate, thanks to the political genius of Mayor Rudy Giuliani and the bonanza of Wall Street’s second Gilded Age. But that’s over—with the suddenness, almost, of 9/11. Mayor Michael Bloomberg, taking office just after terrorists blew a hole in the heart of Gotham’s financial district, let pass the opportunity for radical reform that comes only with extraordinary crises. Now that somber opportunity has come to him again. He can tell New Yorkers that, with the city’s major industry and wealth generator in ruins—with the five great investment banks that seemed so solid having melted into air overnight—the public spending that ballooned on his watch like a financial bubble can’t go on and so won’t. He can say that with 40,000 Wall Streeters losing their jobs, the city workforce will shrink as well. He can say that with their incomes cut, New Yorkers will not face higher taxes to support needless borough presidents’ offices, a redundant civil rights commission, and thousands of other unnecessary “services.”

If ever the time called for a heroic leader, it is now. But as Mayor Bloomberg has already suggested a 7 percent property-tax hike and a 2.5 percent spending cut, God help Gotham.

—Myron Magnet

The new governor, Democrat David Paterson, was a reliable tax-and-spend liberal during his 21 years as a state senator from Harlem. But during his first five months in the governor’s office, Paterson proved a surprisingly strong voice for fiscal responsibility. In August, a month before the financial markets melted down, Paterson warned of a worsening financial crisis and coaxed legislators back to the Capitol for an unusual preelection budget-cutting session.

Their negotiations produced an agreement to cut spending by $1 billion in 2009–10, according to the governor’s estimates. But this reduction was a drop in the bucket. The budget gap for 2009–10 has probably mushroomed beyond $7 billion, over 12 percent of general fund revenues. Indeed, measured by the more rigorous and revealing Generally Accepted Accounting Principles (GAAP) that apply to New York City, the state’s general fund budget is $2 billion in the hole this year.

And Albany’s official budget gap doesn’t include a projected four-year, $6.4 billion operating deficit in the state’s massive Metropolitan Transportation Authority (MTA), which runs the buses, subways, and commuter trains in the New York City metropolitan region. Or the nearly $2 billion unfunded liability in two of the MTA’s three pension plans. Or the $15 billion hole in the MTA’s next capital plan. Or the $8 billion hole in the statewide capital plan for highways and bridges. Or the estimated $47 billion unfunded long-term liability for health coverage promised to retired state government employees.

Gotham’s “Uncontrollable” Crisis

In mid-September, as turmoil shook Wall Street, New York City mayor Michael Bloomberg said that he wanted city agencies—from police to education to homeless services—to cut their budgets by 2.5 percent for the rest of this year and to plan 5 percent cuts for next year, on top of similar cuts announced last year. The mayor also said that he would probably ask the city council to increase property taxes by 7 percent this year, rather than waiting until next year, as was the original plan. But this strategy won’t help Gotham avoid fiscal and social disaster.

Between 2000 and 2007, New York City’s tax revenues grew by a record 41 percent after inflation, yielding an annual increase, toward the end, of more than $11 billion. Most of that money went to support new, permanently higher city spending. Yes, the mayor reserved a few billion for future budget deficits. But once that cushion is gone, the underlying problem will remain: unsustainable spending in areas that Bloomberg considers “uncontrollable.” Over the same period, these areas—debt costs, Medicaid, and pension and health costs for city workers—rose 57 percent, making up 40 percent of the city’s annual $60 billion budget.

The soaring tax revenues that fueled the splurging came, in large part, from Wall Street. Personal and business income taxes, including banking taxes, provided a third of city tax revenues. Finance and real-estate companies were responsible for about a third of the city’s business-tax revenue, while banks (obviously) were responsible for 100 percent of the banking taxes. As for personal income taxes, last year the top 1 percent of taxpayers—those who earned more than $500,000 each—paid 49 percent of them. Many of these taxpayers were, of course, dependent on Wall Street and heavily invested in troubled companies like Lehman, AIG, and Bear Stearns. In short, since the mayor took office in 2002, and since the recovery from the tech bubble and 9/11, the only thing that has stood between the city and a fiscal crisis was Wall Street’s business, now exploded, of structuring and selling off inscrutable securities.

Bloomberg’s focus on “controllable” agency spending means letting the “uncontrollable” parts of the budget continue to swell, even though the money to fund them has disappeared. In two years’ time, whoever is mayor, if he chooses to follow the same strategy, will have to pare the “controllable” budget by at least 15 percent to close a projected $5 billion deficit, even after the 7 percent property-tax hike that’s already in the works. Such cuts could severely damage New Yorkers’ quality of life. Worse, since cutting education by 15 percent is politically unfeasible, other essential departments would bear the brunt. And even those cuts may not be enough, because today’s deficit projections are premised on a quick Wall Street recovery. If that doesn’t happen, the deficits will spiral, possibly by billions.

Cutting the city’s core services to keep funding “uncontrollable” costs would drive away middle-class New Yorkers, risk eroding the tax base, and imperil the gains that the city has made over the past two decades. Instead, the mayor should say publicly that it’s time to figure out how to cut the “uncontrollable” costs. This means working with the state to reform Medicaid so that it does its job—providing humane health care for the poor—without enriching so many special interests. It also means working with Albany and the public labor force to modernize future pension and health-care benefits so that workers pay some of their own health-care premiums and take on some responsibility for their own retirement funds (in well-diversified personal accounts, of course, and with strict oversight and regulation).

Unless Wall Street conjures up a miracle, these steps are the only way to avoid raising taxes (beyond the property-tax hike). And avoiding such tax increases is the best way for New York to attract people from around the country and the world to come and rebuild its economy.

—Nicole Gelinas

Incredibly, Albany managed to go more deeply into debt, increase its long-term liabilities, and shortchange core transportation infrastructure needs even while the good times rolled. So now what? If the past is any guide, Paterson and the legislature will try to muddle through the coming year with a combination of minimal spending restraint, debt-based fiscal gimmickry, fee hikes, and—worst of all—tax increases, in a state already struggling under one of the heaviest tax burdens in the country.

Indeed, Paterson recently wavered on whether he’ll ultimately sign off on the kind of income tax increase that he rejected earlier in the year. Assembly Democrats, under the leadership of Speaker Sheldon Silver, have passed two versions of a “millionaire tax” this year, the latest of which would raise the top rate by nearly 2 full percentage points. The new Senate Republican leader, Dean Skelos of Long Island, has flatly rejected any tax hikes. But the Republican Senate majority may not survive a Democratic tide in the November elections.

There’s a better way out of this crisis. Prior to the Wall Street storm, the numbers indicated that Paterson could close the gap and balance his budget merely by holding spending growth to zero next year. The erosion of revenues caused by the meltdown means that he will now have to slash state-funded expenditures by at least 2 to 3 percent. It’s been done before—most recently by Pataki, in the mid-1990s.

Plenty could be saved by downsizing state agencies, and there’s money to be raised in the short term from selling or privatizing assets. But with nearly three-quarters of his budget dedicated to Medicaid, public schools, and other local assistance, Paterson can’t begin to eliminate next year’s gap merely by nibbling around the edges of state operations. The main targets are obvious: school aid, which would rise by $2 billion under the current spending formula; and Medicaid, projected to increase another $1.7 billion.

But spending restraint in the coming year isn’t remotely enough to get New York finances under long-term control. New York must reduce permanently the size and scope of its public sector. Paterson and the legislature need to give New York City mayor Michael Bloomberg and other local government leaders the tools they need to manage more efficiently. That should start with a sweeping reform of the Taylor Law, which sets the terms of collective bargaining on terms overly favorable to public-employee unions. Paterson must also take the lead in proposing a major reform of public pensions and a restructuring of costly and unfunded health benefits for government retirees.

Instead of hammering what’s left of its economy with new taxes, New York needs a bold strategy for promoting growth. Two decades of industrial policy, in the form of targeted economic development grants and public works, haven’t revived the upstate economy or stemmed the region’s continuing population losses. Paterson should instead propose significant new tax breaks for New York investment—and, to jump-start the upstate economy, something truly dramatic, such as the phased elimination of corporate taxes north of the mid-Hudson region, as the business group Unshackle Upstate has suggested.

Above all, though, Paterson has to recognize that Wall Street isn’t in just another cyclical downturn. In effect, the state government has been skimming the profits of a gigantic casino packed with drunken gamblers. Now the casino has shut down permanently, and what replaces it will be more like a sedate church bingo hall. That’s going to require Albany to make a radical adjustment to its expensive and expansive lifestyle.