In mid-February, just seven weeks into office, New York City Mayor Zohran K. Mamdani delivered somber news to state legislators: the city faces a $5.4 billion deficit for the fiscal year beginning July 1, the result, he said, “of budgetary failures of the past.” Even after spending cuts, he argued, the state should raise income and business taxes and transfer the proceeds to the city immediately—“the most direct route out of this budget crisis.” Thankfully for New Yorkers, the mayor was mostly bluffing: this year’s budget gap is manageable, and the city faces no acute emergency.

But Mamdani’s push unwittingly raised a graver point: If things are this strained when the global, state, and local economies are nominally doing all right, and when city tax revenues are therefore rising, what would happen if the city entered a recession—historically, a matter not of if but when?

Finally, a reason to check your email.

Sign up for our free newsletter today.

No modern New York mayor, save for Mamdani’s one-term predecessor, Eric L. Adams, has avoided a downturn, and the economy is overdue for one. Aside from the sharp unemployment spike caused by the Covid-19 lockdowns in the spring of 2020, the U.S. economy has not experienced a normal cyclical recession since 2008, nearly two decades ago. And no modern mayor is less equipped than Mamdani to grapple with an economic and fiscal crisis.

The city faces deeper problems than the 34-year-old mayor’s inexperience and his ideological resistance to what he calls “austerity”—that is, serious budget cuts. More consequential are Mamdani’s expansive governing ambitions, including $9 billion in new annual local spending on everything from universal child care to a Department of Community Safety to free buses. For now, because he has no way to finance these initiatives from existing revenues, the mayor left most of that new spending out of his initial budget proposal.

Even before Mamdani’s election, New York City had begun to convince itself that local government could run its own mini–welfare state, as several major programs—now swelling inexorably—make clear. The city has come to believe that it can be all things to all comers, even as potential constraints on tax-revenue growth loom. And Mamdani has inherited a jobs base that, compared with previous economic expansions, is growing too slowly to sustain the city’s existing commitments, let alone its ambitions.

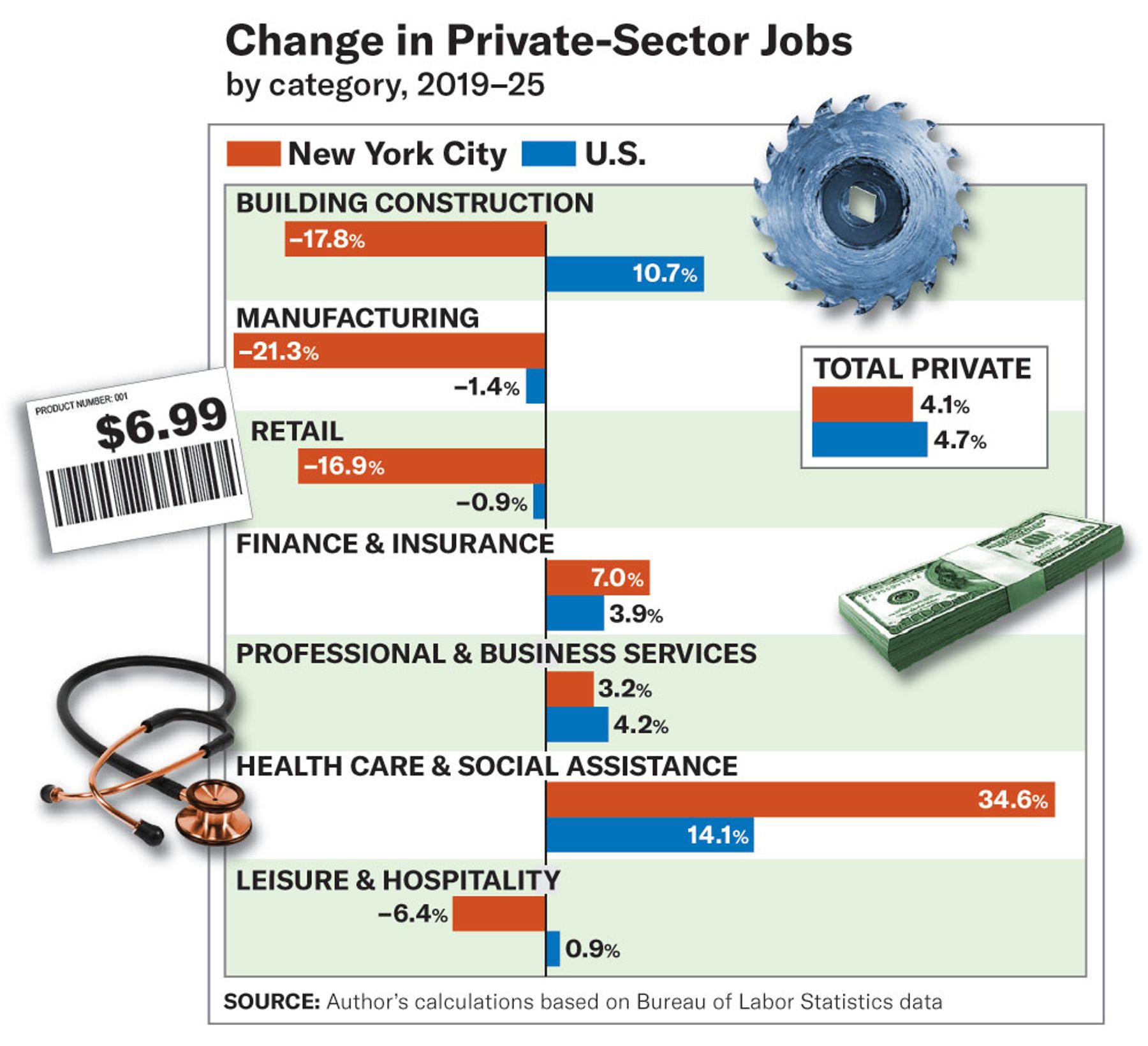

New York City’s economy looks reasonably healthy—if you don’t look too closely. As of December 2025, the city boasted more than 4.3 million private-sector jobs, an increase of 4.1 percent from December 2019, before the Covid-19 lockdowns, an average gain of about eight-tenths of 1 percent per year. Average weekly wages, at just under $1,500, are up 11 percent over the same six-year span.

But these numbers pale in comparison both with the nation as a whole and with the city’s own recent past. Over the same six years, the United States has added 4.7 percent more jobs, and wage gains have been far stronger: 29.5 percent, comfortably exceeding the cumulative 26.1 percent inflation rate during this period. New York is also losing ground in high-earning employment. Just over six years ago, on the eve of the pandemic, the average American earned 73.5 percent of the average New Yorker’s wage; today, the average American earns 87 percent of that wage, according to my calculations based on Bureau of Labor Statistics data.

As for Gotham’s modern economic history, between 1990 and 2000—the bookends of two economic peaks—the city added 6.6 percent to its private-sector jobs base, an average of seven-tenths of 1 percent yearly. Between 2000 and 2008, another pair of peaks, it added only 2.6 percent, or about three-tenths of 1 percent annually. The city more than made up for this sluggish growth, however, between 2008 and 2019, adding a remarkable 25.1 percent in new private-sector jobs—an average of 2.1 percent per year. The slower pace since then marks a return to an earlier era, before the hyper-tourism and tech boom that defined the 2010s.

One final note of sobriety: the mix of New York’s job growth has increasingly tilted toward lower-paying positions, many of them supported directly or indirectly by taxpayer spending—one reason wage gains have been so modest. Some of this shift is long in the making. For decades, the city has been losing its share of the nation’s highest-paying investment-related jobs, falling from 33 percent of the national total in 1990 to just 18 percent today, according to state figures. The city counted about 201,500 such jobs in 2024, only 400 more than a quarter-century earlier. More troubling still, even without a recession, New York lost some of these positions last year, while rival financial centers in Florida and Texas continued to add them. In Texas, the 97,100 jobs in this sector represent 27.4 percent growth since 2019; national statistics don’t break out this category for Florida, though it appears to be expanding quickly there as well. J.P. Morgan now employs more people in Texas than in New York, notes the Partnership for New York City, a business-lobby group, and a new stock exchange in the Lone Star State is likely to attract even more high-value economic activity.

New York is also struggling to keep pace with the nation in maintaining a broad base of lower-paying, entry-level positions that, unlike the lower-wage health-care jobs that have increased in recent years, don’t depend on government subsidies. The city once excelled at creating such jobs. The city has yet to recover the retail and hospitality jobs lost during the pandemic, with employment in those sectors still down 16.9 percent and 6.4 percent, respectively. Some of this reflects long-term shifts in the economy; but nationally, those jobs have largely returned. In corridors of downtown and Midtown, many former mid-priced restaurants have given way to “slop-bowl” outlets and fast-food joints where, increasingly, customers order from automated kiosks—and even that business is starting to contract.

The city’s broader economic mood isn’t helping. “Employment growth in the city is not strong,” says Steven Fulop, the former Jersey City mayor who recently became chief of the Partnership, in part “because of the rhetoric and the language” surrounding last year’s campaign and the new mayoralty. “You’ve had four taxes proposed in two months. . . . When leadership talks the way it’s talking, it creates uncertainty.” The surest way to reduce inequality, Fulop argues, is straightforward: “Growing paychecks, growing jobs”—something the city “is not doing right now.”

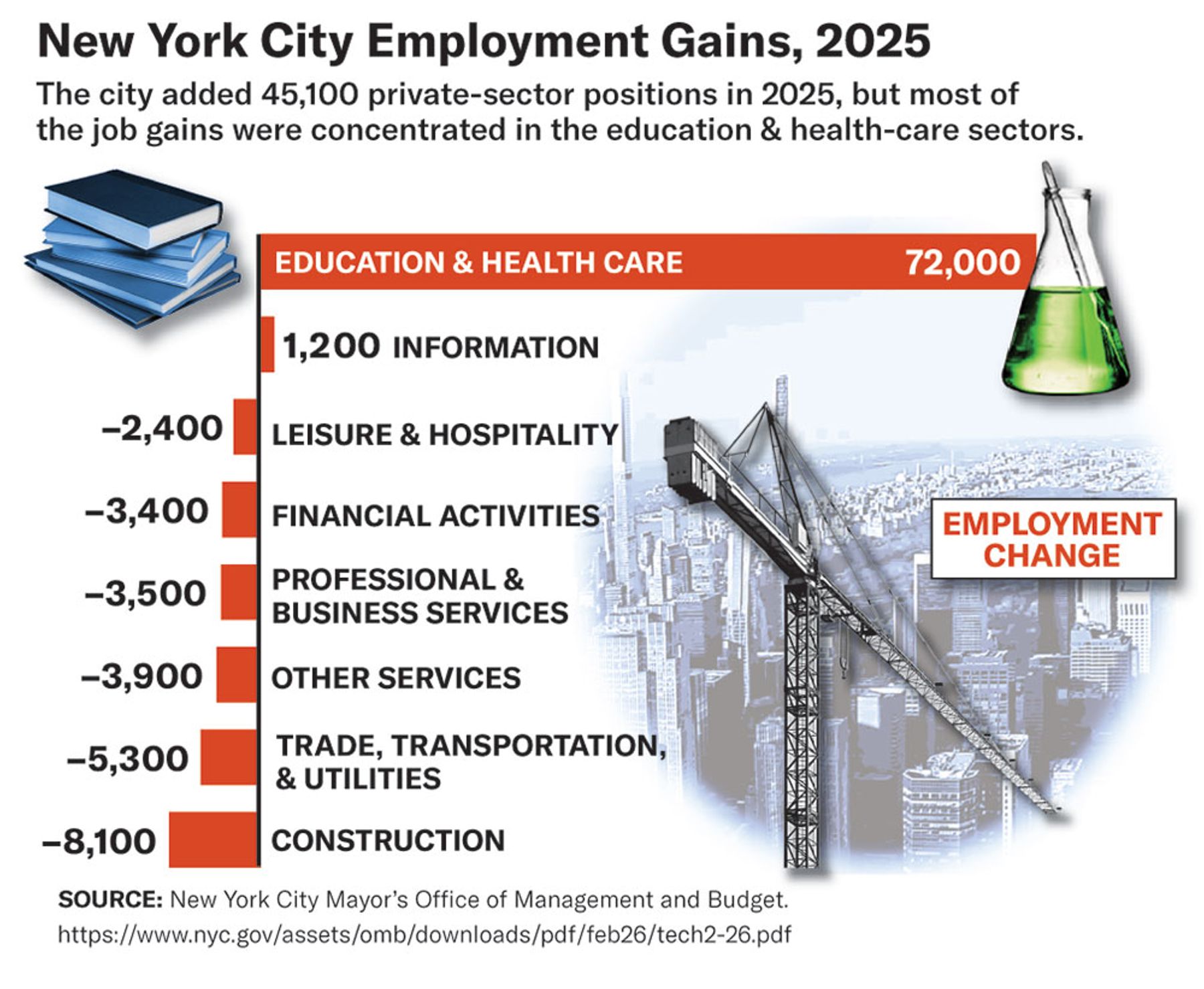

New York’s already-sluggish labor market may now be stalling entirely. A striking chart in Mamdani’s first budget presentation in February shows that the city lost employment across nearly every major sector last year—from leisure and hospitality to professional services—except one: the heavily subsidized education and health-care sector.

It’s hard to escape the conclusion that New York’s decade of higher taxes, combined with heavy mandates on business, including a minimum wage that has reached $17 an hour, has begun to catch up with its economy. In 2021, the state raised its top income-tax rate, so that households earning more than $323,000 now face combined state and local rates ranging from 10.7 percent to 14.8 percent. In the past half-decade, Governor Kathy Hochul and state lawmakers have twice raised a payroll tax on New York City employers—literally a tax on jobs—to help fund the region’s transit system. If these high costs are restraining growth now, with businesses not yet in full cost-cutting mode and wealthy residents not nursing major market losses, how much more damage might they do in a downturn?

The city’s recent budget expansion tells a different story from its weak job numbers. Even as employment has lagged and the city’s share of national income has slipped, tax and fee revenues continue to rise. The city expects to collect $97.6 billion in its own revenues in the fiscal year beginning this summer (federal and state grants make up most of the remainder of the $127 billion budget). That figure is up from $67.5 billion in 2019; unlike wages, revenues have more than kept up with inflation.

This surge reflects the city’s reliance on high-earning residents, workers, and visitors. New York draws on more than a dozen taxes—from a levy on commercial rents to a tax on cannabis—but four sources dominate: property, sales, and personal- and business-income taxes. Property taxes, falling on everyone who owns or rents property, are the largest single source, expected to bring in $40.3 billion next year. Sales taxes add another $11.4 billion. The fastest increase, though, has come from income taxes. Revenue from personal-income taxes has risen to $21.3 billion from $13.3 billion in 2019; from business-income taxes, to $7.3 billion from $4.3 billion over the same period.

That’s partly because the city’s bankers may be fewer in number, but they, as well as others in their income cohort, are earning more. As state comptroller Thomas DiNapoli reported last year, Wall Street directly accounted for 7 percent of city tax revenue in 2024 (and an even larger share, 19 percent, of state revenue). Thanks to bankers’ outsize spending, the industry also supports about one in 11 city jobs—from restaurateurs to jewelers—and generates 17.7 percent of overall economic activity. Beyond Wall Street, other wealthy residents also earn, and pay, a disproportionate share of the city’s income and taxes. Recent city figures show that just 1.2 percent of households (those earning over $1 million annually) pay about 38.3 percent of city income taxes, slightly above their share of total income. In 2023 alone, these households accounted for nearly $5.6 billion of the $14.6 billion that the city collected in income taxes.

Are New York’s rising taxes harming the city’s broader economy? The answer is not academic, as the Citizens Budget Commission notes that the city has steadily lost its share of the nation’s millionaire earners, falling from 6.5 percent to 4.2 percent between 2010 and 2022—a decline that represents a loss of political, economic, and job-creating power.

That this decline hasn’t been highly visible doesn’t mean it’s not being felt. Andrew Sidamon-Eristoff, a former New York City finance commissioner and state tax commissioner, observes that “businesses and other advocates for lower taxes routinely oversell the simplistic assertion that people physically move in response to high taxes. That’s not quite how it works.” Instead, he argues, “with careful planning and a few lifestyle changes, taxpayers can still hold on to their . . . Manhattan apartment but avoid New York taxes on their investment income” by spending most of their time outside the city and state. “The proportion of high-income New York taxpayers who file New York returns as non-residents”—people who maintain a presence in the city but do not reside here for tax purposes—“has been trending up for decades,” Sidamon-Eristoff adds, a pattern noted by the Manhattan Institute’s E. J. McMahon. In a recession, as both banks and people reliant on investment income look to cut costs, this trend could accelerate.

Economists predict recessions far more often than they occur, and in recent years they have speculated endlessly about when and why the next one might arrive. Would it come from the bursting of an AI bubble? Or, paradoxically, from AI working too well, reducing the need for white-collar workers? (Indeed, the number of openings for new college grads is down.) Or would the downturn resemble the 2008 crash—a collapse in credit conditions, after years in which lending and borrowing were far too easy?

The precise cause of a future recession matters less than its consequences for New York. An immediate effect—especially if Wall Street were involved—would be a sharp drop in revenues. The city’s income-based taxes, highly sensitive to economic activity, are also its most volatile sources of revenue. During the 2008–10 downturn, for example, the city lost 24.4 percent of its personal-income-tax revenues. A comparable decline today would cost it about $5.2 billion annually—doubling the current deficit that Mamdani has described as a crisis requiring tax hikes.

Corporate-tax revenues—another volatile, though smaller, source—fell by 35.5 percent from their $3.1 billion peak during that same period. A similar drop today would mean another $2.6 billion in lost revenue, bringing the additional shortfall to roughly $7.8 billion. Sales-tax revenues shrank only slightly in that downturn, and property-tax revenues did not fall at all. Even so, combining all these other recessionary losses with the city’s existing deficit would produce a gap of roughly $13.2 billion—about 13.4 percent of city-funded revenues—leaving officials to choose between tax hikes at exactly the wrong moment or sweeping spending cuts.

A recession would also bring significant lost employment. After the global financial crisis nearly two decades ago, New York shed 3.2 percent of its jobs; a comparable decline today would mean roughly 139,000 lost positions. Even so, the city fared relatively well in that episode, thanks largely to the massive Wall Street bailouts undertaken by the Bush and Obama administrations. (For different, highly unusual reasons, the far larger job losses of 2020 offer little guidance as a precedent.)

A similar rescue today would be far from certain. Political hostility toward the globalized financial sector has hardened over the past two decades, and a president who routinely disregards the “expert” advice that earlier administrations followed might prove reluctant to intervene. The federal government’s fiscal capacity is also more constrained: printing trillions of dollars in emergency aid, as Washington did during the 2008 crisis and the pandemic in 2020 and 2021, would now risk reigniting inflation.

The greater long-term jobs threat, though, lies in deeper technological and location shifts already reshaping the city’s labor market. New York has watched this process unfold for decades in Wall Street employment and, more recently, in leisure and retail. A recession would likely accelerate the trend, pushing employers to automate and relocate work more quickly, with AI further hastening the shift.

With short-term revenue losses and long-term job erosion squeezing the city’s finances, how would New York scale back? Any cuts to basic public services—from policing to sanitation—would be complicated by a broader trend: the city’s transformation into a provider of automatically expanding entitlements and redistributive social spending. The two core social-services agencies (Social Services and Homeless Services) have seen their spending explode from $12.3 billion in 2019 to a projected $19.3 billion in 2027, rising from 13.3 percent to 15.2 percent of the budget. “The problem with the budget is that there are structural issues,” says the Partnership for New York City’s Fulop. “Even if you raise taxes on the highest earners,” he continues, “any additional revenues will be absorbed quickly by additional programs that are unsustainable.” In a downturn, he adds, “your budget has to be at a place where it can sustain adverse economic conditions.”

Two social-services programs are ballooning rapidly. In 2023, the city council expanded a seven-year-old initiative with the unwieldy name City Fighting Homelessness and Eviction Prevention Supplement (CityFHEPS), which helps pay rent for New Yorkers at risk of entering the shelter system. The rationale was that rental vouchers would save money by reducing shelter stays, but the program’s loose eligibility criteria mean that hundreds of thousands of city families could soon qualify. Spending on the program has risen from $25 million in its first year to $700 million in the current fiscal year to $1.6 billion for the next fiscal year—and a conservative estimate has it hitting $2.6 billion in 2030.

Another long-standing program, cash welfare—once thought to be permanently reduced after 1990s-era reforms to the federally funded portion—has similarly blown up, with caseloads rising from fewer than 150,000 in 2019 to more than 300,000 by late last year; these and other “public-assistance” costs (not including health care) have expanded from under $1.6 billion in 2019 to nearly $2.8 billion next year. Mamdani’s biggest specific complaint about these programs, though, is not that Adams failed to curb their growth but that he failed to set aside money for them. Which raises the obvious question: What money—even during the relatively good times?

There’s a reason that local governments rarely run expansive social-welfare systems, regardless of ideology: such programs tend to swell during recessions. Unlike the federal government, which can borrow—though perhaps not to the extent that it has in the past two decades—to meet rising need, city governments generally cannot, and should not, finance downturn spending through debt. At the same time, redistributive programs rely on taxes paid largely by higher earners and businesses, the very revenues most sensitive to economic cycles. Those revenues often fall just as demand for aid rises. As Paul Francis, a longtime Cuomo administration veteran who recently founded the Step Two Policy Project to address the state’s health and human-services challenges, puts it: “The question of, ‘Can you do these things at a local level?’ is a serious one. At some point, you outstrip your revenue base.”

How could New York better prepare for a recession? First: avoid making matters worse. Mamdani’s proposed state tax hikes on the city’s wealthy earners and businesses would deepen the city’s reliance on its most volatile revenue sources. “Ensuring these taxes don’t pass is the job of the governor,” says Francis, who argues that Albany must take “the long-term view” and “the statewide view” of the city’s tax base. Governor Hochul has so far resisted Mamdani’s push and, he suggests, should continue to do so. “It’s just not good governance.”

The city must recognize, too, that it has already hit the limit of how much it can redistribute, as opposed to funding basic services. Mamdani himself is encountering those limits now. In his inaugural budget, he couldn’t reserve funding for his Department of Community Safety or for free buses, simply because the money wasn’t there. Even with Governor Hochul agreeing to fund the launch of universal child care, that program’s rollout will be far more gradual than Mamdani suggested during the campaign. And that’s not a bad thing: an extrapolation of early figures suggests that, in part because of New York’s high service-delivery costs, child care just for all two-year-olds would cost $2.2 billion.

Finally, the city must recognize that its mounting stack of mandates, including the $17 minimum wage, is harming job growth. The city council now proposes raising that wage to $30 by 2030. Mamdani has been circumspect about the idea—and for good reason. He should continue to resist it.

New York need not wait for a recession to learn an old lesson: even wealthy cities cannot function as engines of redistribution. A city’s first duty is to provide basic public services, and when expanding social spending threatens those services, everyone—including the poor—pays the price. The warning signs are already visible. That New York’s socialist mayor is sounding alarms about a budget crisis before any downturn suggests that the city’s fiscal structure is already under strain. If and when tighter times arrive, New York may quickly discover how sensitive residents and businesses become to ever-higher taxes and regulations.