When I was a young adult, living with your parents was considered a sign that your life had veered off-course. Perhaps you had lost a job or had broken up with a partner and needed to reset or to save some money before getting back on your feet. Whatever the cause, a stigma attached to living with your parents, which counted as a big negative in the dating market. But it seems like norms have changed, and living with your parents is now seen as just another way to save money.

I recently spent a few hours watching personal-finance advice on Tik Tok for a column. I was pleasantly surprised to find that much of the advice was sensible. But what surprised me was how common it was to suggest to young adults that they should live with their parents—not because their lives had fallen apart, but to save money. “Why pay rent?” viewers were asked (though the influencers encouraged viewers to contribute to household expenses).

Finally, a reason to check your email.

Sign up for our free newsletter today.

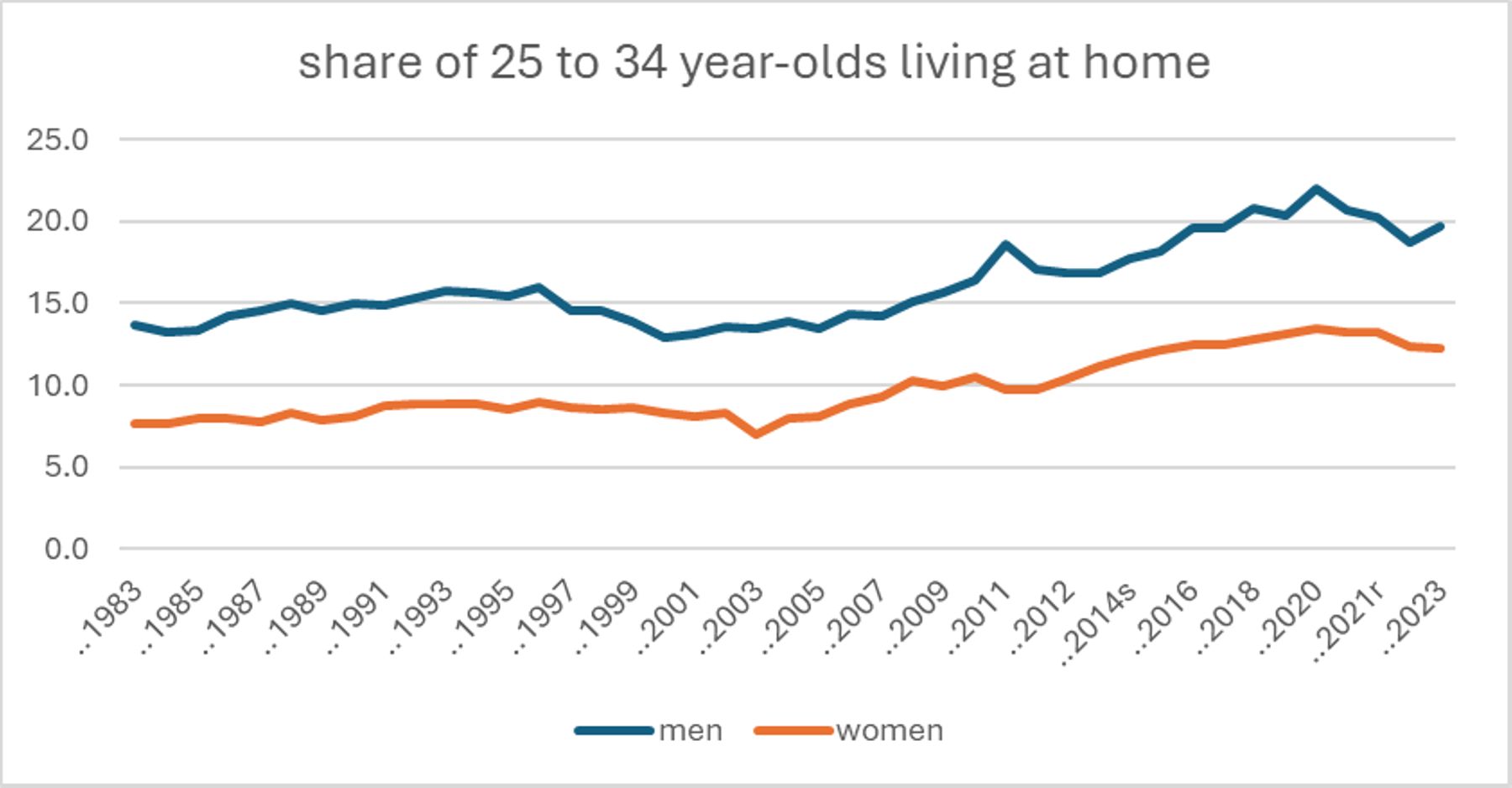

Those viewers are listening. The share of 25- to 34-year-olds living with their parents has creeped up over the years. Doing so was extremely popular during the pandemic, and while many young adults eventually left the nest, the proportion living with their parents remains high compared with historical levels.

If you ask Gen Zers why they’re living with parents, they’ll probably say that it’s because things are harder these days (as every generation believes). They have a point, though: rents are very high relative to income, especially in desirable cities. Student debt is also more pervasive than ever before, and those loan payments are eating into Gen Zers’ incomes and making housing less affordable.

Still, while these are valid excuses, they don’t explain the whole trend. Student-debt holders also tend to earn higher incomes because they got more education. In fact, having a big student loan is correlated with owning a home. And the income-based repayment plan has become more popular and accessible in recent years. It ensures that even if you take on tens of thousands of dollars in loans and then choose a low-paying career right out of college, student-loan payments won’t overwhelm your meager salary.

It’s also true that rents are higher than ever. But living with your parents isn’t the only alternative: you can get roommates or move to a cheaper city; people still have choices. Living at home is more socially acceptable, and even desirable, for some people today. This is in line with other cultural changes over the years. Young adults grew up friendlier with their parents, speaking and texting with them more frequently because of mobile phones. They also grew up less interested in independence and behaved less rebelliously as teenagers. They didn’t individuate to the same degree as earlier generations. These trends reinforce the social norms that we’re seeing now.

In theory, there is nothing wrong with this trend. Living with parents well into adulthood is common in Europe. Until the mid-twentieth century, it was normal to live with your family until you started out on your own. This was especially true for young women. Spending more time with one’s family has much to recommend it, of course.

But there are drawbacks, too. Living with one’s parents can signal less risk-taking and independence, which have negative connotations for personal development and for the broader economy. It’s also notable that living at home has become much more common for young men at the same time that they are less likely to work or to marry. It’s not clear which way the causality goes: in some cases, men can’t find work (though in this tight labor market, that explanation seems dubious); or perhaps the option of living at home enables one to work less and never fully launch as an adult. Paying rent is a great impetus to advance your life and career.

When I watched the videos of financial influencers suggesting that people live at home, I couldn’t deny that they had an economic point. I recalled all the money I spent on terrible apartments in my twenties. Rent took up more than half my income as an economics Ph.D. candidate living on a merger stipend in New York City. Perhaps I would be able to afford a better apartment today if I had stayed home longer. But my 25-year-old self would probably have said that some things are more important—that while I was spending money I might otherwise save, I was also making an investment in vital life skills.

Photo: Maskot/DigitalVision via Getty Images