In March, the Consumer Price Index (CPI), the most cited inflation metric, rose more than forecasters expected for the third month in a row. Though the Federal Reserve prefers a different measure—the Personal Consumption Expenditures (PCE) Price Index—the string of hot CPI reports has called into question whether annual inflation will keep falling to the Fed’s 2 percent target. It also raises doubts about the Fed’s current plan of cutting its target interest rate three times this year. Right now, year-over-year CPI and PCE inflation stand at 3.5 percent and 2.5 percent, respectively.

The CPI and PCE are indices of the entire price level for consumer goods and services. Each consists of subindices that look at specific sectors (for example, everything from food to clothing to housing to health care) or strip out other sectors from aggregated data (for example, “core” inflation, which omits changes in food and energy prices). For the past three years, economists and others have debated which of these measures best predicts future inflation. Unfortunately, both can be misleading.

Finally, a reason to check your email.

Sign up for our free newsletter today.

There are at least three reasons for this. First, it’s hard to know in real time whether a change in prices reflects a change in supply, a change in demand, or both. Consider energy prices, which have risen substantially this year and have contributed to CPI-measured inflation. Many observers point to new demand from energy-intensive data centers, which power artificial intelligence. On the other hand, supply shocks, such as bad weather in the United States and attacks on both Russian and Ukrainian oil refineries and power plants, have also caused oil and gasoline prices to rise.

In the first half of 2008, the Fed faced a similar conundrum when it had trouble discerning whether high oil and commodity prices reflected heightened demand or temporary supply shocks. High prices caused the Fed to worry excessively about inflation as the economy contracted. Had the agency not been influenced by the supply shocks’ price effect, it might have pursued a more expansionary monetary policy earlier that year and mitigated the Great Recession. Volatile energy costs are a big reason many economists prefer to look at core inflation measures, though even those include some spillover, since energy is an input for the production of other goods.

Second, whenever aggregate demand in the economy is excessive (that is, when there is “too much money chasing too few goods”), certain prices will spike more than others at any given time—but that doesn’t mean those specific prices are the cause, rather than the symptom, of inflation.

For example, car insurance saw large price increases that contributed significantly to the March CPI number. Economist Omair Sharif points out that car parts have become expensive over the past few years, making car insurance costlier. Though those higher prices feed into the CPI and PCE, economist Scott Sumner observes that this confuses a change in a relative price (a price of one good or service in terms of another) with a change in the overall price level. More expensive car parts can lead to more expensive car insurance, but that need not cause the overall cost of living to rise, as long as the pricier parts are offset by declines in inflation elsewhere.

Suppose you have a fixed monthly budget, but this month you need to pay a higher premium for car insurance. You now have less money for the other goods you normally buy. Therefore, the quantity you demand of those other things will decline. Assuming many other people are in the same boat, they will also be unable to afford as many of those other goods, and those prices will fall. But when the overall price level rises for an extended period, we have good reason to blame excessively stimulative monetary and fiscal policy.

Third, housing (or shelter) prices, which have also contributed much to recent inflation, are tough to measure, especially when home prices are changing rapidly. The CPI does not measure actual home prices. Rather, the Bureau of Labor Statistics (BLS), which publishes the CPI, measures rents from a sample of rental units and “owners’ equivalent rent” (or OER)—that is, how much a homeowner estimates he would charge for renting his home. In measuring actual rents, the BLS samples about 48,000 units, divided into six panels. Then, the BLS rotates through the six panels each month, so each gets surveyed every six months. Though this approach is reasonable, it suffers from a significant measurement lag.

In addition, OER is based on homeowners’ best guesses, not observable data. Economist Arin Dube finds that, if we subtract OER from CPI, then CPI inflation is already at 2 percent. For Dube, the inflation surge is effectively over. By contrast, economist Jason Furman finds that “core services excluding shelters,” a metric that avoids the problems of measuring rent and OER, has been ticking up and could portend a re-acceleration of inflation.

As we can see, myriad ways exist to slice and dice inflation data. Measurement challenges make it hard to trust inflation data, and supply shocks complicate interpretation. That’s why the better strategy for the Fed to ensure that inflation does not reignite is to pay less attention to price indices and more to total spending in the economy and nominal wage growth.

The most cited measure of total spending is nominal gross domestic product (GDP). Since real (inflation-adjusted) GDP is equal to nominal GDP adjusted by the price level, nominal GDP growth is equal to real GDP growth plus inflation.

If the Fed targeted nominal GDP growth, it would allow inflation to fluctuate in response to changes in real GDP growth (supply shocks), while still anchoring inflation over time. Moreover, if the Fed were primarily concerned about nominal growth, it would not need to worry about whether changes to the price level were coming from supply or demand shocks. It would only worry about keeping spending growth stable.

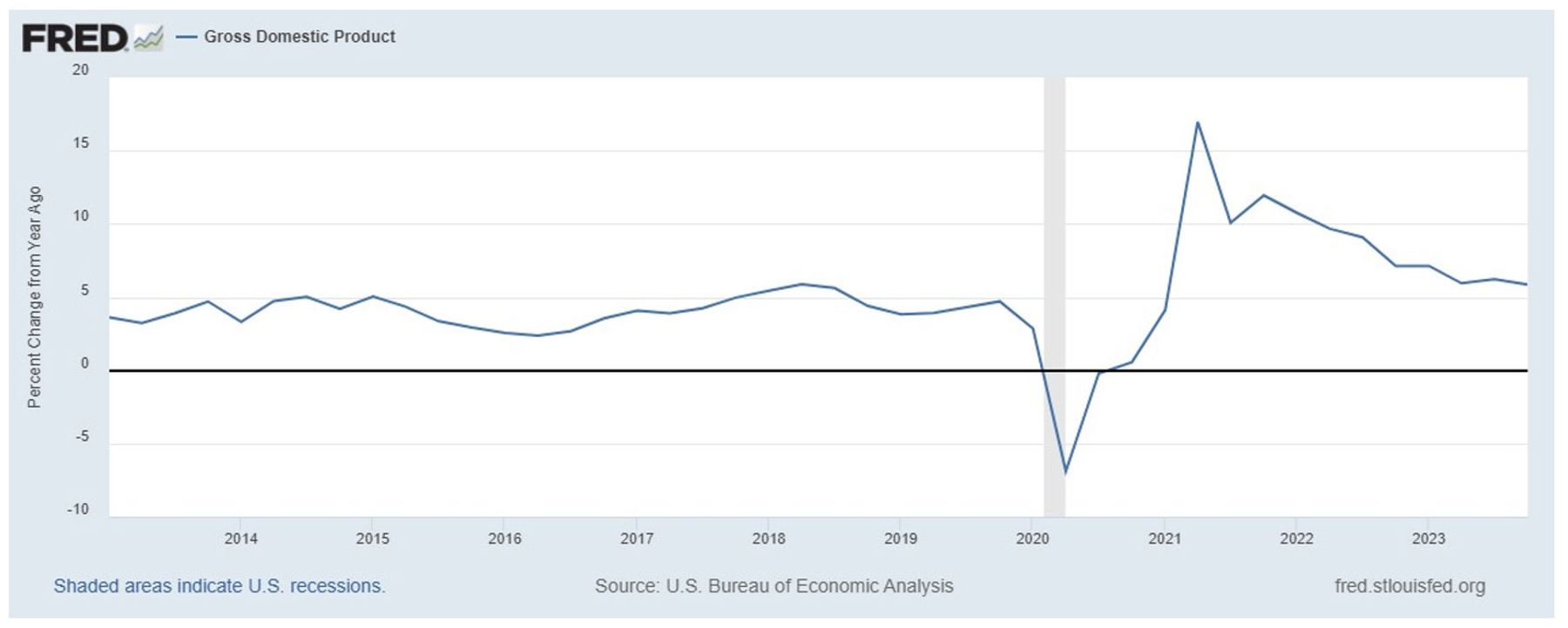

Year-over-year nominal GDP growth has been very high since the first quarter of 2021. The rapid growth was initially appropriate, as the economy was recovering from the steep recession a year earlier—but nominal GDP soon overshot its pre-pandemic trend. With so much spending growth in the economy, it’s no wonder that inflation has been so high. As the figure from Federal Reserve Economic Data below shows, though nominal GDP growth has slowed, it remains high compared with the 2010s. As of the last quarter of 2023, year-over-year nominal GDP growth was 5.9 percent.

True, nominal GDP comes with its own measurement challenges. It is subject to revision and data on it come out only quarterly. For these reasons, policymakers should also consider nominal wage growth. A steep decline in wage growth typically means the economy is contracting and falling into recession, while soaring wage growth usually suggests excess aggregate demand and higher inflation. Nominal wage growth closely tracks nominal GDP growth, but it also comes out at a monthly frequency.

The next figure, also from Federal Reserve Economic Data, shows a three-month moving average of wage growth. Like nominal GDP growth, wage growth has fallen considerably since peaking in summer 2022, but it is still high relative to where it was pre-pandemic. As of March, the three-month average was 4.9 percent.

The best strategy the Fed can pursue to bring inflation down sustainably would be to drive nominal GDP and wage growth down to 4 percent, roughly the rate both grew during the stable late-2010s. Recent data suggest we’re already gradually heading in that direction. On the other hand, these trends show past data, not forecasts of where these variables are expected to go. Reasonable people can disagree about the best way to forecast total spending and wage growth, but until we have that conversation, we may be stuck arguing about flawed measures of the price level and not the actual source of inflation: excessive stimulus.

Photo: Tom Williams/CQ-Roll Call, Inc via Getty Images