After peaking at 7 percent in June 2022, inflation has fallen dramatically in the United States. In November, year-over-year inflation clocked in at 2.6 percent, as measured by the Federal Reserve’s preferred Personal Consumption Expenditures price index. December PCE data will come out Thursday, setting the stage for what the Fed hopes will be the final act of its tightening cycle.

While inflation remains above the central bank’s 2 percent target, many “Team Transitory” economists view last year’s progress as vindication of their claim that inflation was mostly driven by pandemic- and war-related supply shocks, not by excessively loose monetary and fiscal stimulus. Most Team Transitory members believe inflation would mostly have fallen without the Fed’s interest rate hikes of the past two years. Their views contrast with those of former Treasury secretary Larry Summers and those of “Team Permanent,” who argued from the outset that inflation had to be swiftly addressed.

Finally, a reason to check your email.

Sign up for our free newsletter today.

Both sides hope that 2024 delivers a “soft landing,” with inflation reaching the 2 percent target without the economy falling into recession. But the Fed must still be vigilant to prevent inflation from reemerging. While Team Transitory has (so far) been correct that inflation could fall with limited economic pain, the Fed should reject its claim that the inflation surge was primarily supply-driven. If the central bank fails to understand the role that excess demand played in the inflation surge, the United States could face economic instability later this year.

At first, the Fed accepted the supply-shock narrative. When inflation took off in spring 2021, for example, the central bank maintained that inflation “largely reflected transitory factors.” Even by September of that year, the central bank forecast that it would keep its target interest rate (the federal funds rate) at zero through 2021, raising it only 25 basis points (a quarter of a percentage point) in 2022. It projected 3.4 and 2.1 percent annual inflation for 2021 and 2022, respectively.

Annual inflation outstripped those predictions, however, hitting 6.2 percent and 5.4 percent, respectively, in 2021 and 2022. Fed chair Jerome Powell adopted a more hawkish tone in November 2021, but he kept the federal funds rate at zero through the end of the year. That forced the Fed to play catchup: from March 2022 to today, the central bank has raised the federal funds rate 525 basis points.

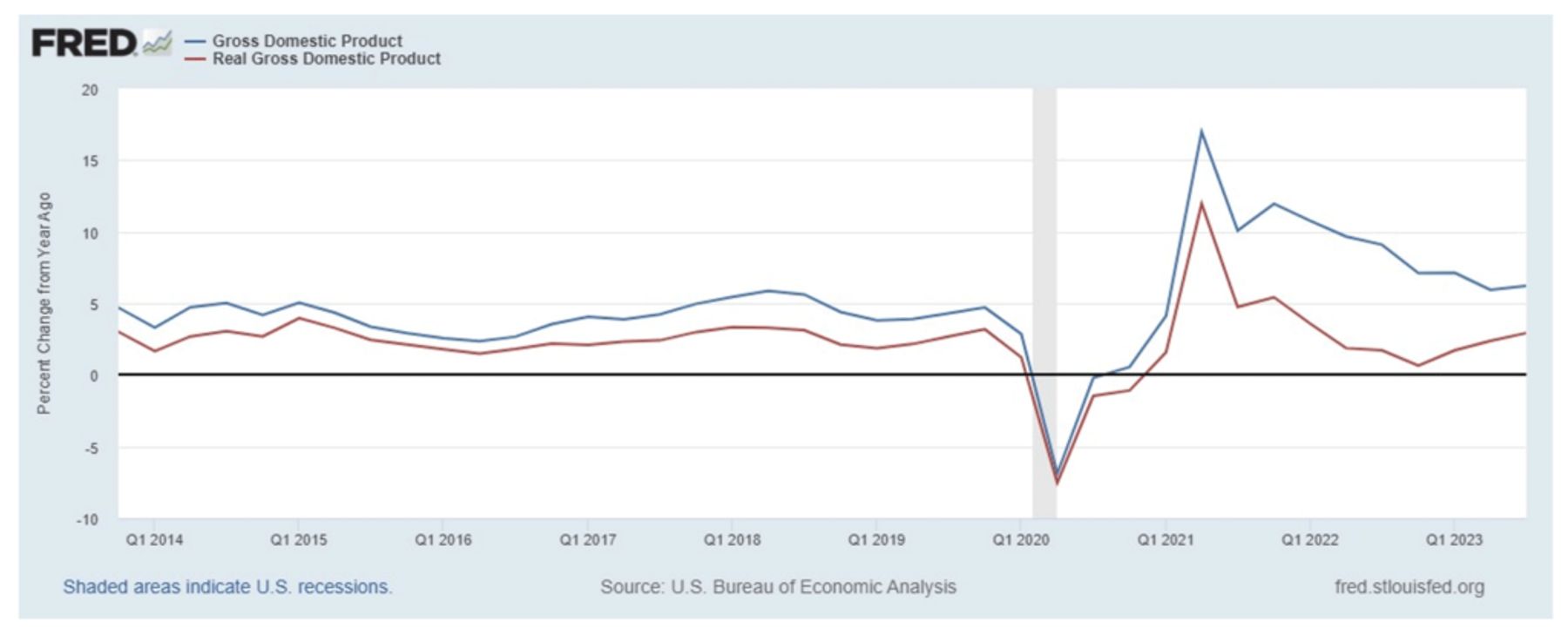

These developments seemed to undermine Team Transitory’s argument. To see why, consider the “aggregate demand–aggregate supply” model of the economy. Aggregate demand refers to total spending in the economy; aggregate supply refers to inflation-adjusted economic output. Economists typically use nominal gross domestic product—the sum of spending on final goods and services in today’s prices, not adjusted for inflation—to measure aggregate demand, while they use real (inflation-adjusted) GDP to measure aggregate supply. Real GDP helps give a sense of the total volume of goods and services in the economy from year to year.

All else held equal, a negative supply shock, such as the pandemic or the Russia–Ukraine war, will reduce output and raise prices, while a positive aggregate demand shock, such as the Fed’s monetary policy or the 2020 and 2021 stimulus checks, will raise both output and prices. A negative supply shock could, theoretically, increase, decrease, or maintain the nominal GDP. But even if the shock raised nominal GDP, the increase likely would be minor because prices and output would be moving in different directions. By contrast, positive aggregate demand shocks historically have significantly raised nominal GDP.

If the inflation surge of 2021 and 2022 had been mostly supply-driven, we would have seen a fall in real GDP growth and little to no change in nominal GDP growth. That’s not what happened.

The Federal Reserve Economic Data figure below shows the past decade’s year-over-year real and nominal GDP growth. Since 2021, nominal GDP growth has well exceeded its 2010s levels. Real GDP growth similarly rose sharply in 2021, and while it slowed down in late 2022, it picked up again last year. Despite warnings from Team Transitory that rate hikes were overkill, the economy kept running hot. It’s unlikely we’d be seeing such a booming economy if inflation had only come from supply shocks.

This is not to say that Team Permanent got everything right. Though Larry Summers accurately warned that inflation would become a major problem, he also predicted the U.S. would need to suffer a major rise in unemployment—anywhere from a one-year spike to 10 percent unemployment to five years of 6 percent unemployment—for inflation to be fully vanquished. Instead, the unemployment rate ran below 4 percent for nearly all of 2023. Even if unemployment increases this year, Summers’ prediction is unlikely to come true.

Summers made his flawed prediction based on the Phillips Curve, which sees a tradeoff between unemployment and inflation. While unemployment typically does go up after a period of high inflation, it won’t necessarily always do so. Whether unemployment will rise after inflationary periods depends on the public’s expectations. If workers believe inflation won’t fall any time soon, they will keep demanding higher (nominal) wages. In this case, the Fed is struggling to show credibility, so it must resort to a surprisingly tighter monetary policy to convince the public that it is serious about bringing inflation down.

Such a surprise slows total spending more than expected and eventually brings down inflation. It also increases unemployment, because employers will be unable to offer the higher wages that workers have come to expect. As economist George Selgin has pointed out, the Fed’s struggle to convince the public it was serious about controlling inflation in the late 1970s was a major reason that unemployment steeply rose when inflation eventually came down. On the other hand, if the public believes that the central bank is committed to bringing down inflation, workers will not demand such large wage increases. The Fed can then slow spending growth without necessarily causing unemployment to rise.

Fortunately, despite initially falling behind the curve, the Fed has retained sufficient credibility as an inflation-fighter. The central bank’s actions, coupled with the fading of pandemic- and war-induced supply shocks, have brought inflation down without causing major harm to the labor market. Nominal GDP growth is still too high to reach 2 percent inflation, however. In the third quarter of 2023, nominal GDP growth was 6.2 percent; to achieve the Fed’s inflation targets, that figure needs to fall closer to its pre-pandemic level of roughly 4 percent.

Last month, the central bank signaled that it might cut the federal funds rate in 2024. If nominal GDP growth keeps shrinking, this course of action could turn out well. But if demand does not sufficiently cool, the Fed should hold off on cutting rates, lest it risk another bout of rising inflation.

Photo: Douglas Rissing/iStock